Health AI distribution build vs. buy — Phreesia primer (Part 1 of 2)

A profitable public incumbent with ~4,700 clinics and ~180M patient visits a year trades at ~1.3x forward sales, while the AI-native startups chasing the same buyers raise at 40 to 100x. The incumbent may be fairly priced as a stock. Its distribution, though, may be worth far more to an acquirer than to public shareholders. A primer on Phreesia, the numbers, and the build-vs-buy question that gap sets up.

Health AI Distribution: Build vs. Buy, Part 1 of 2. This piece is the primer and the strategic-asset case. It covers what Phreesia is, why the public market prices its distribution cheaply, and why that distribution may be worth far more to an AI-native acquirer than to public shareholders. Part 2 of the series (“Health AI distribution build vs. buy — illustrative math”) works the numbers: what that distribution would cost an AI-native company to build on its own, the combination economics (CLTV, the payments rails, a grounded re-rating), and the deal mechanics (reverse merger, PIPE, the IPO window, precedents).

How to read this. This is a point-in-time company analysis as of late June 2026. Phreesia’s fiscal year ends January 31, so “FY2026” is the year ended Jan 31, 2026. Valuations and private ARR move monthly, so treat the figures as point-in-time and the structure of the argument as the takeaway. Private-round valuations are primary-market marks, not mark-to-market, and are not directly comparable to a public enterprise value. This is analysis, not investment advice.

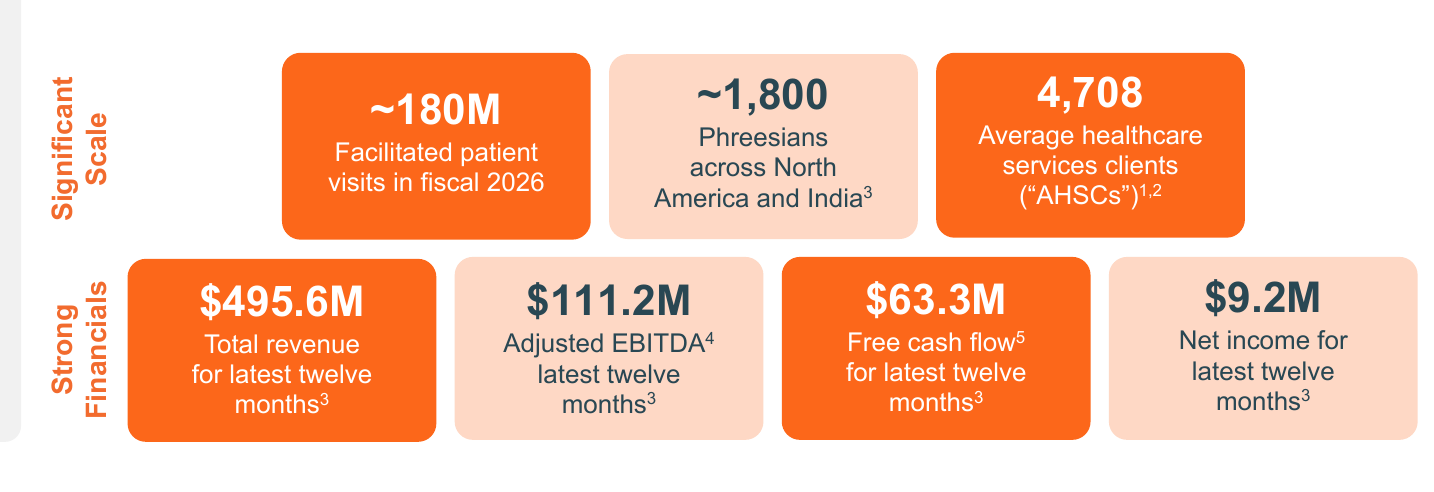

Healthcare has a company that already sits at the front desk of roughly 4,700 provider organizations, facilitates about 180 million patient visits a year, generates positive free cash flow, and just crossed into nominal GAAP profitability. It is publicly traded, so you can buy the whole thing for an enterprise value of about $683 million, roughly 1.3 times its forward revenue guide. Meanwhile, venture investors are paying 40 to 100 times revenue, sometimes more, for private startups that do one slice of what that company does, at a fraction of its scale.

The incumbent is Phreesia (NYSE: PHR), a profitable, cash-generative public company whose stock has fallen out of favor. It is down from a 52-week high near $33 to roughly $10. The insurgents are the AI-native patient-access players clustered around Silicon Valley venture capital: companies like Assort Health, Luma Health, and Hyro, among a broader cohort of voice-AI and ambient players. The distance between how the public market prices the incumbent and how the private market prices the insurgents is the thing to watch in this corner of health tech, and it sets up a classic strategic question. This piece lays out the business, the financials, the installed base, and the valuation gap, then works through what that gap implies.

One clarification up front, because it changes how to read everything below. Phreesia’s standalone stock may well be priced correctly. Its single-digit growth and cyclical, pharma-funded ad revenue probably justify a low multiple. The argument here is narrower and strategic. The distribution trading inside that cheap multiple is worth far more to an AI-native acquirer that needs it than to public shareholders pricing the incumbent on its own trajectory.

Phreesia company primer

Phreesia (NYSE: PHR) runs a vertically integrated patient-intake and “patient activation” platform that digitizes the administrative front end of the care encounter: discovery and scheduling, registration, eligibility and benefits, patient payments, and engagement. It serves roughly 4,700 healthcare organizations spanning health systems, hospitals, and ambulatory/specialty groups. It sits at a high-frequency chokepoint in the workflow, touching ~180M patient visits in FY2026 (on its own framing, roughly one in six U.S. patient visits), and earns money off that position through three revenue streams. Read it as a scaled, sticky distribution platform. Monetization is diversified and partly counter-cyclical, and margins and free cash flow have just turned the corner.

Exhibit 1. Phreesia at a glance. Source: Phreesia Q1 FY2027 investor presentation (slide 5).

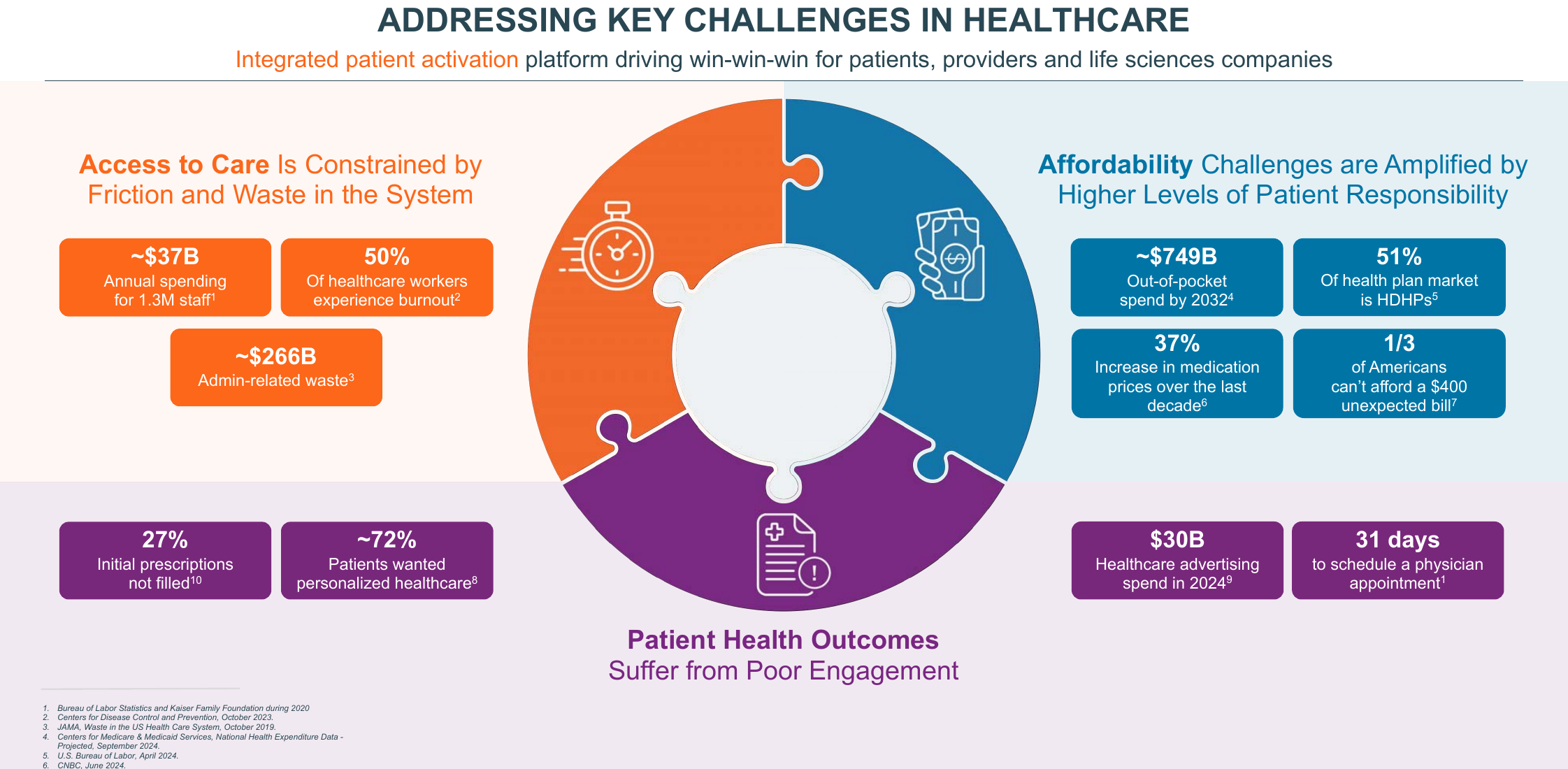

The platform is positioned against three structural frictions in U.S. healthcare delivery that management frames as a “win-win-win” for patients, providers, and life sciences: constrained access (administrative friction and an estimated ~$266B of admin-related waste), affordability pressure (rising out-of-pocket responsibility and high-deductible-plan adoption), and weak patient engagement and outcomes.

Exhibit 2. Industry backdrop. Source: Phreesia Q1 FY2027 investor presentation (slide 6).

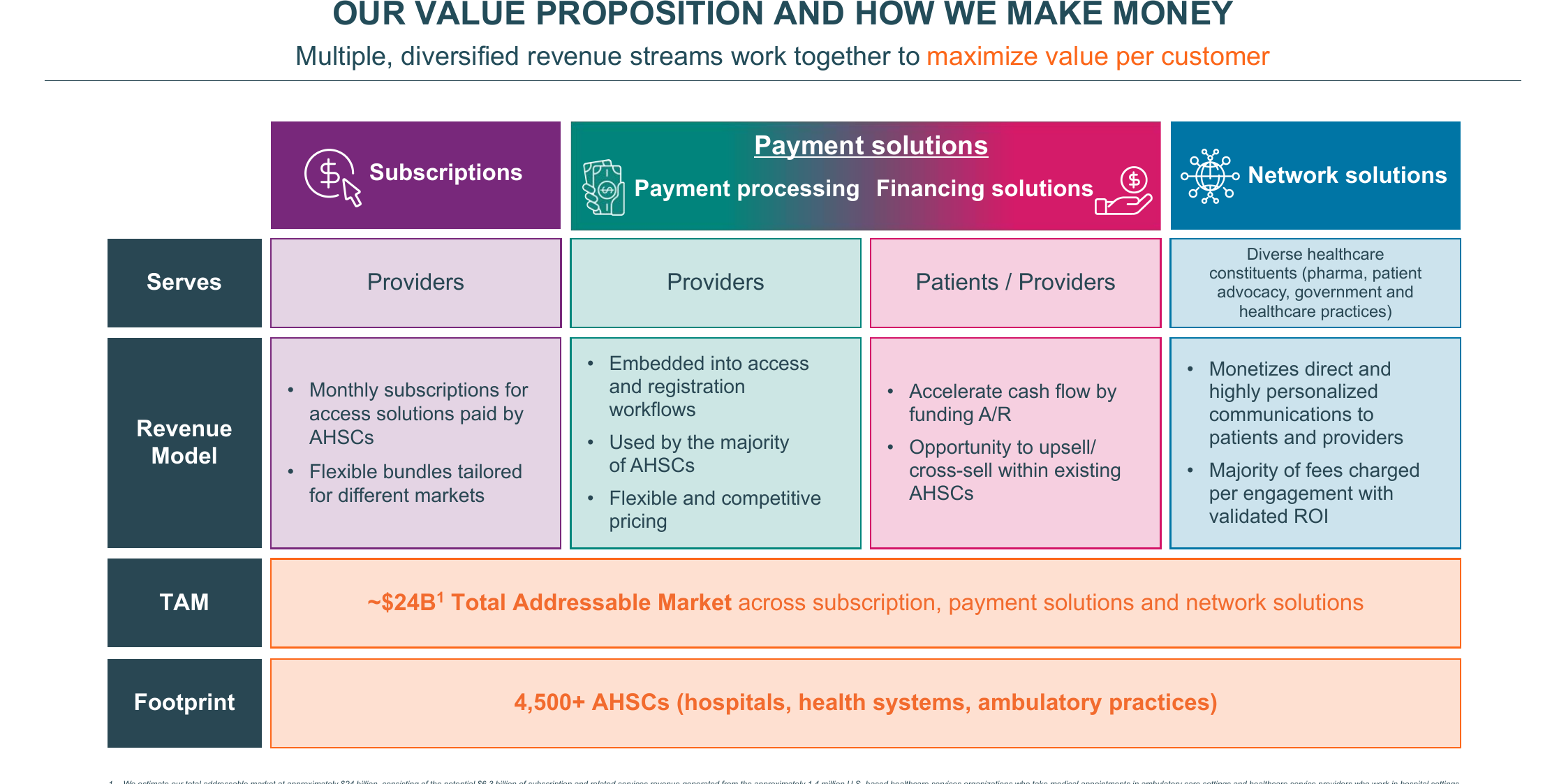

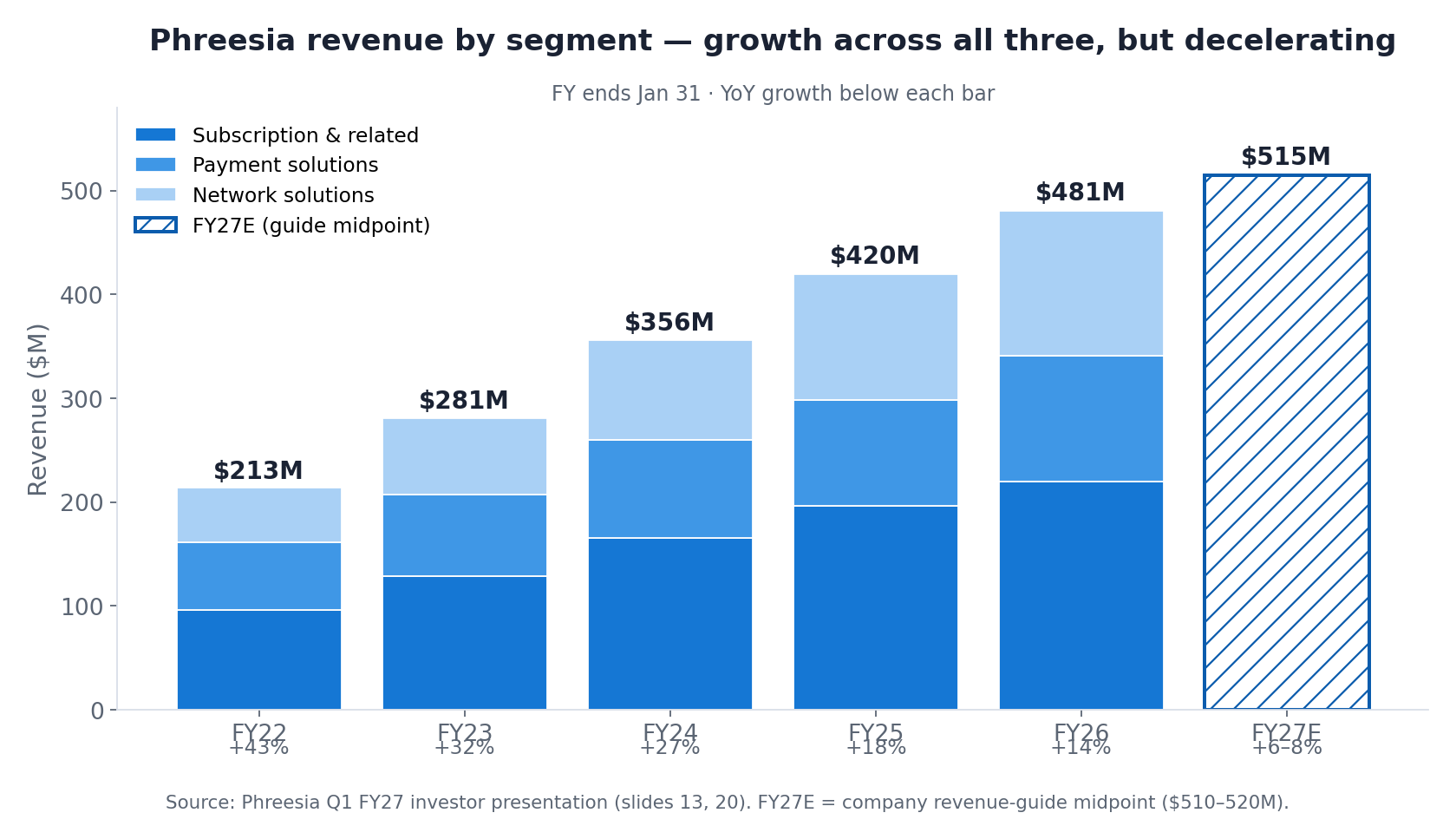

Revenue is reported in three segments that share a single customer relationship but carry distinct growth, margin, and cyclicality profiles. Subscription & related is the recurring software anchor. Payment solutions monetizes patient-payment volume embedded in the same workflow, and since the November 2025 ~$160M acquisition of patient-financing company AccessOne, patient financing too. Network solutions sells targeted, point-of-care communications funded by life sciences and pharma. That line carries high margins, runs cyclically, and is the source of the FY2027 guidance reduction. For FY2026 the mix was ~46% subscription, ~25% payments, and ~29% network; Phreesia does not disclose segment-level margins.

Exhibit 3. How Phreesia makes money. Source: Phreesia Q1 FY2027 investor presentation (slide 8).

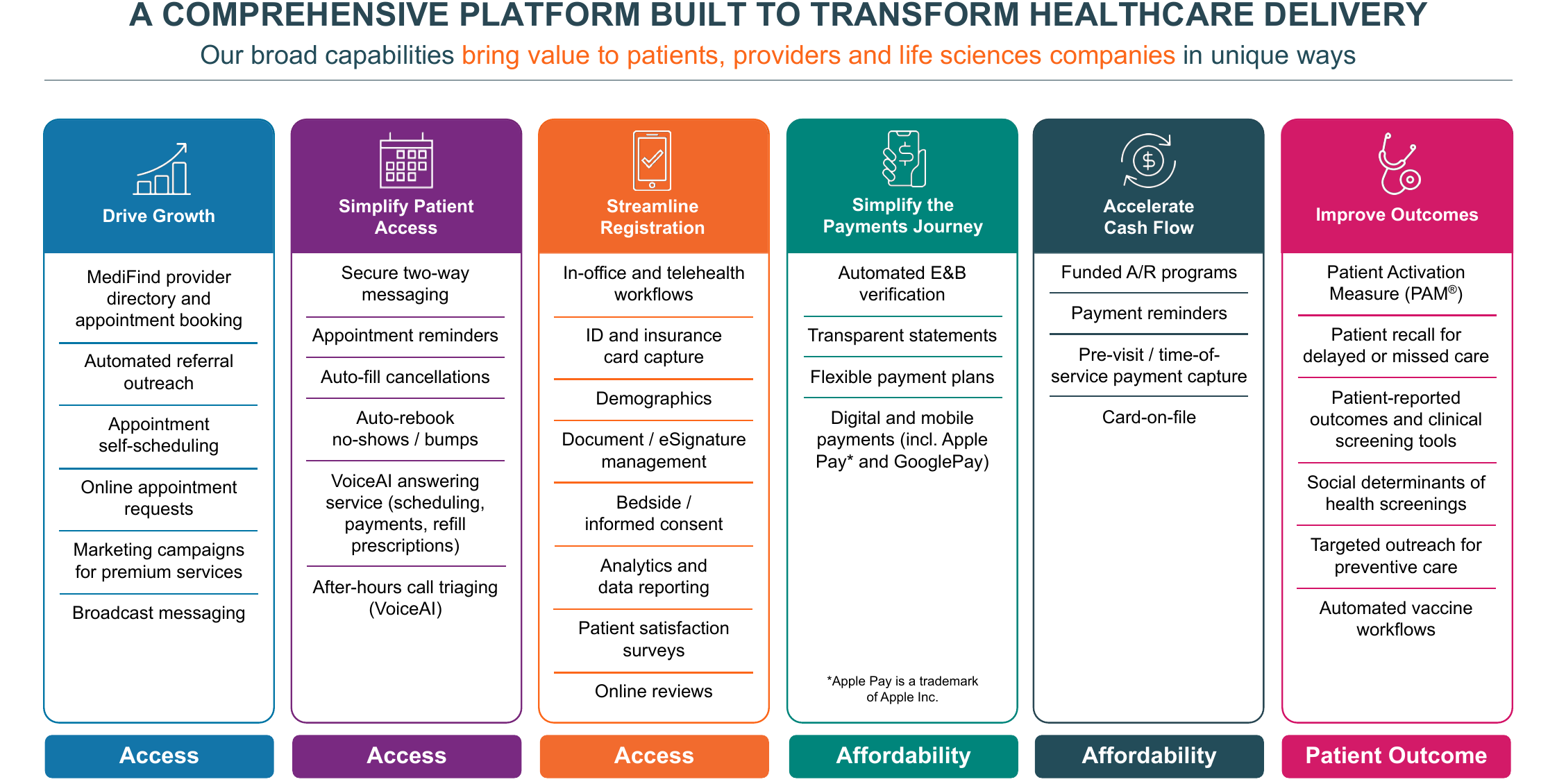

The land-and-expand motion is simple: land with software, then grow wallet share across payments and network monetization inside the installed base. That is the mechanism behind Phreesia’s rising revenue per client. The platform spans the full patient and revenue-cycle journey, which deepens switching costs and opens several cross-sell paths per account.

Exhibit 4. Platform capabilities. Source: Phreesia Q1 FY2027 investor presentation (slide 7).

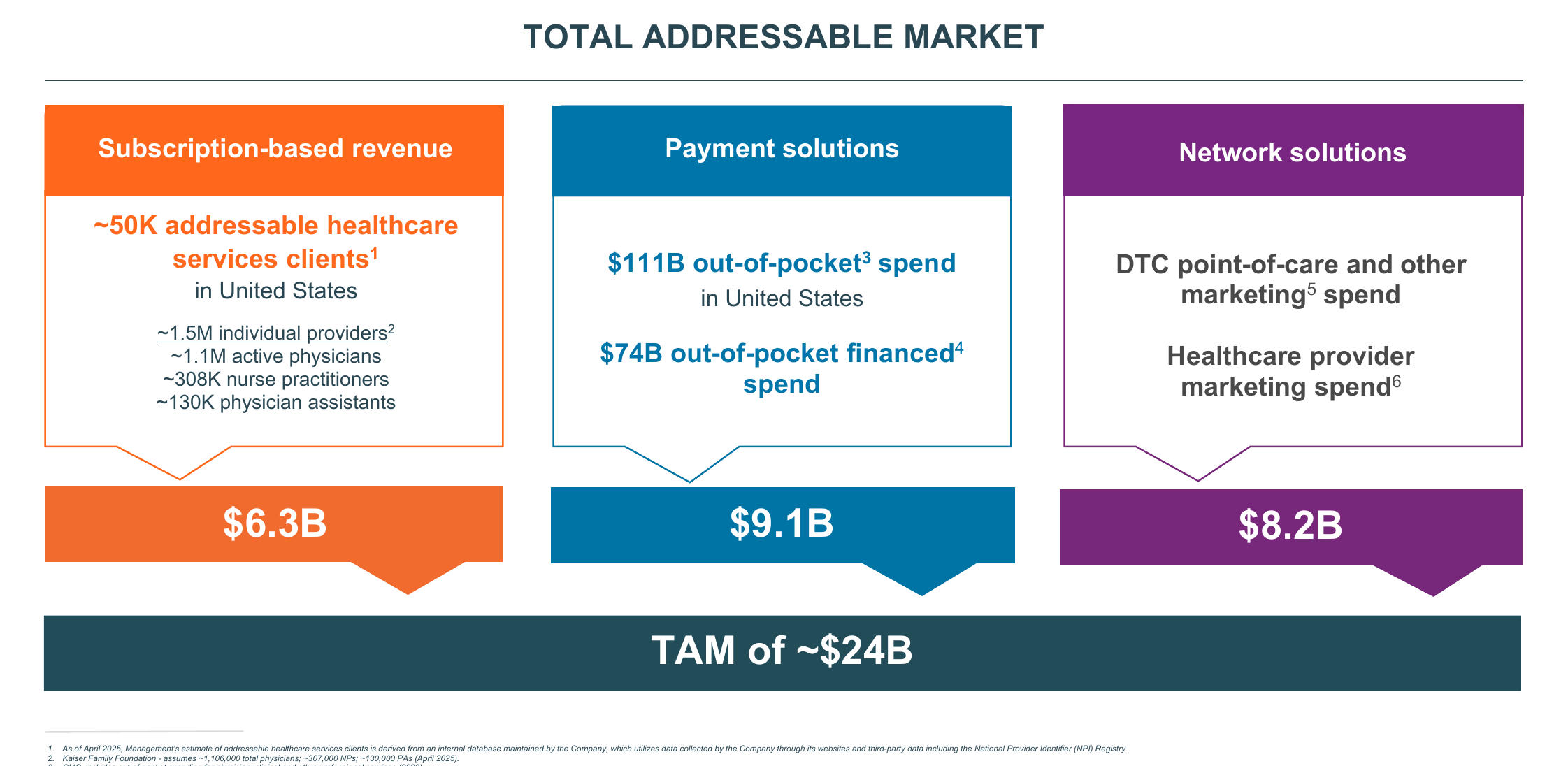

Management frames an aggregate TAM of ~$24B across the three segments: ~$6.3B subscription, ~$9.1B payments, and ~$8.2B network, against ~50,000 addressable healthcare-services organizations and ~1.5M individual U.S. providers. Set against ~$481M of FY2026 revenue, that implies low-single-digit penetration (~2%), leaving a long reinvestment runway even as the reported growth rate decelerates.

Exhibit 5. Total addressable market (~$24B). Source: Phreesia Q1 FY2027 investor presentation (slide 23).

The financials: growth is real, but decelerating

Phreesia has compounded revenue from $213M in FY2022 to $481M in FY2026, with every segment growing. The growth rate has stepped down hard, from +43% to +14%, and management guides FY2027 to just +6% to +8% ($510M to $520M), after cutting the top of the range from $545M to $559M on softer pharma/network demand.

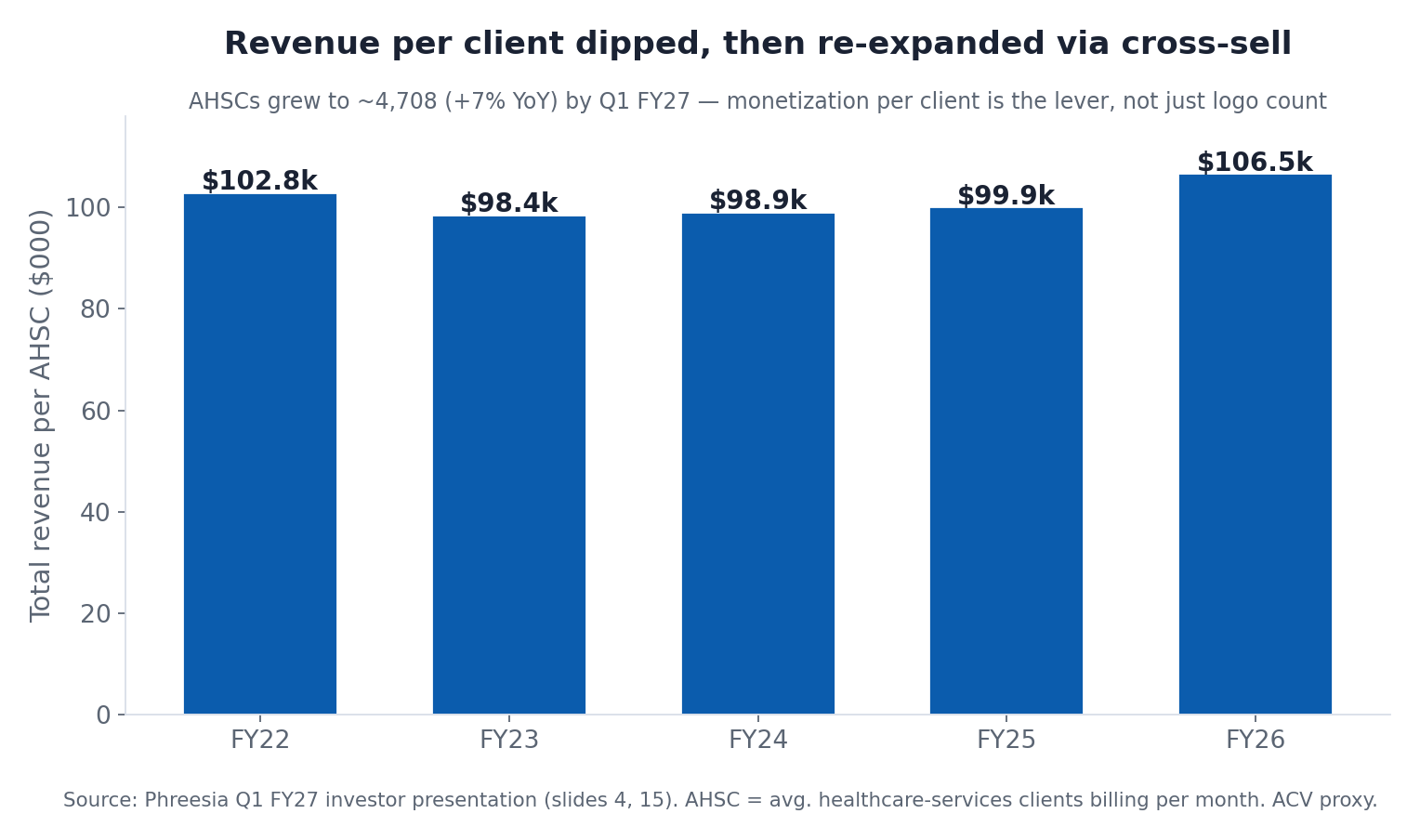

Underneath the headline number, the per-client story runs ahead of what the deceleration suggests. Total revenue per AHSC dipped as Phreesia added smaller clients, bottomed near $99k, and has re-expanded to $106.5k as payments and network cross-sell deepened. Management is explicit that it is not optimizing the subscription line. It is moderating software price on purpose to capture higher-value downstream payment and network transactions per client. The client count itself keeps grinding up (4,708 AHSCs in Q1 FY2027, +7% year-over-year), with mid-single-digit growth guided ahead.

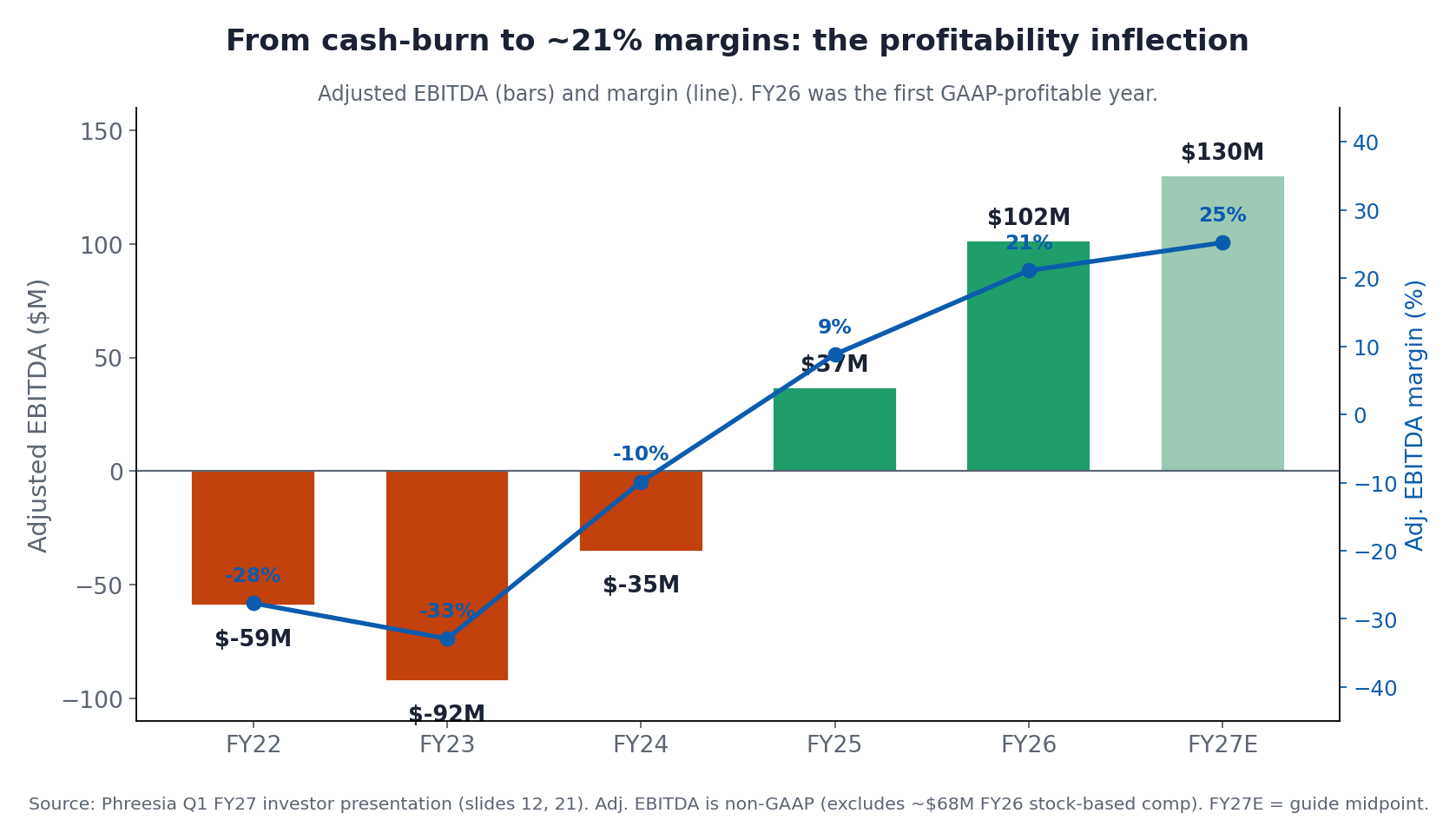

The bigger transformation is on profitability. Phreesia spent years buying growth. FY2026 was the inflection. The company swung from deeply negative adjusted EBITDA to $101.5M (21% margin) and its first GAAP-profitable year ($2.3M net income), with guidance to $125M to $135M of adjusted EBITDA (~25% margin) in FY2027.

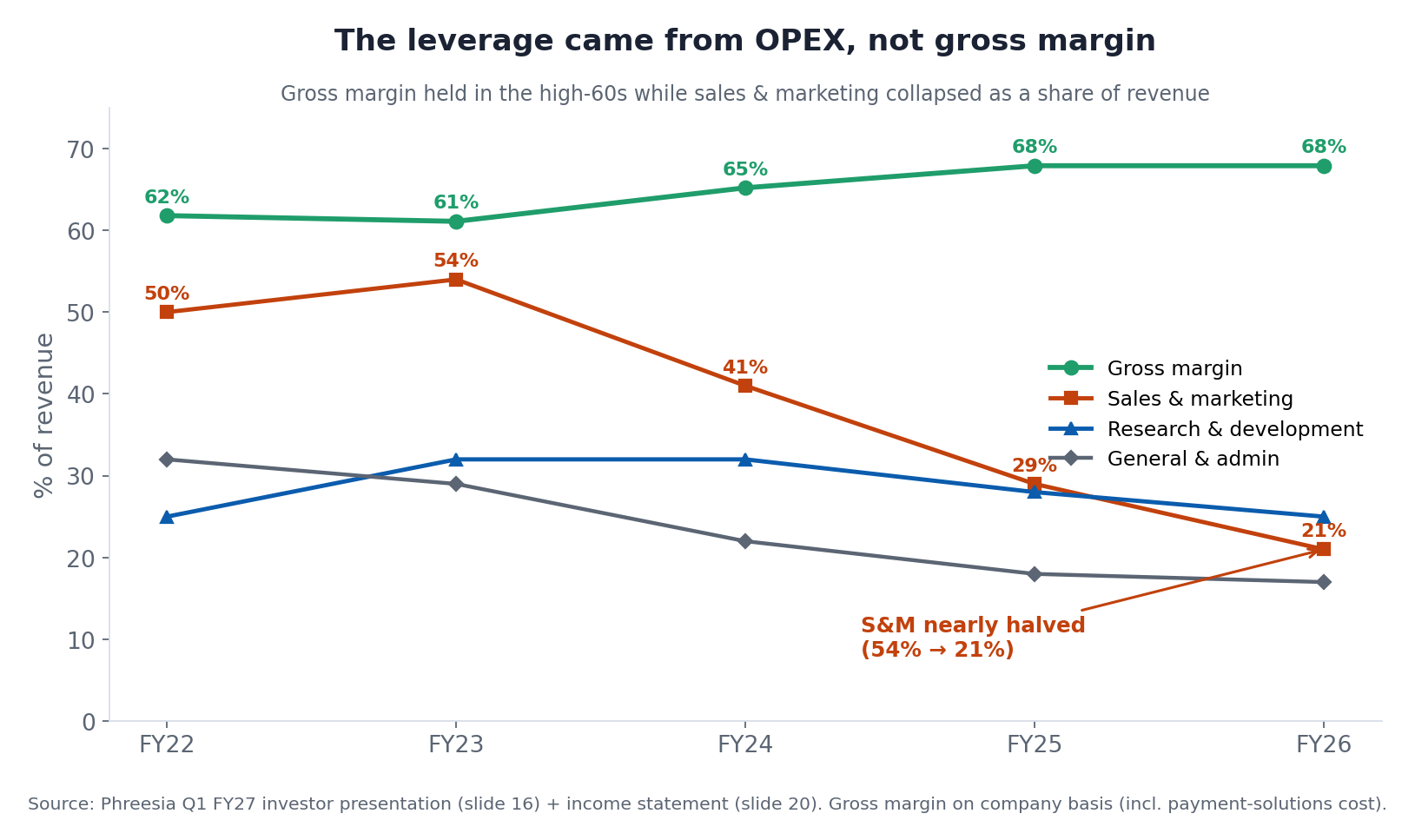

That margin expansion came from operating leverage rather than gross margin, which has sat in the high-60s the whole time. Specifically, sales & marketing collapsed from 54% of revenue to 21% as the company shifted from land-grab to harvest. This is the signature of a maturing platform: a stable, high-60s gross margin and a cost base that finally scales.

One caveat sits underneath the “adjusted” numbers. Stock-based compensation ran ~$68M in FY2026 (about 14% of revenue). On a GAAP basis, counting that comp, EBITDA was ~$25M, not $101.5M. That gap is likely one reason the stock screens cheap on GAAP earnings, and we’ll come back to it.

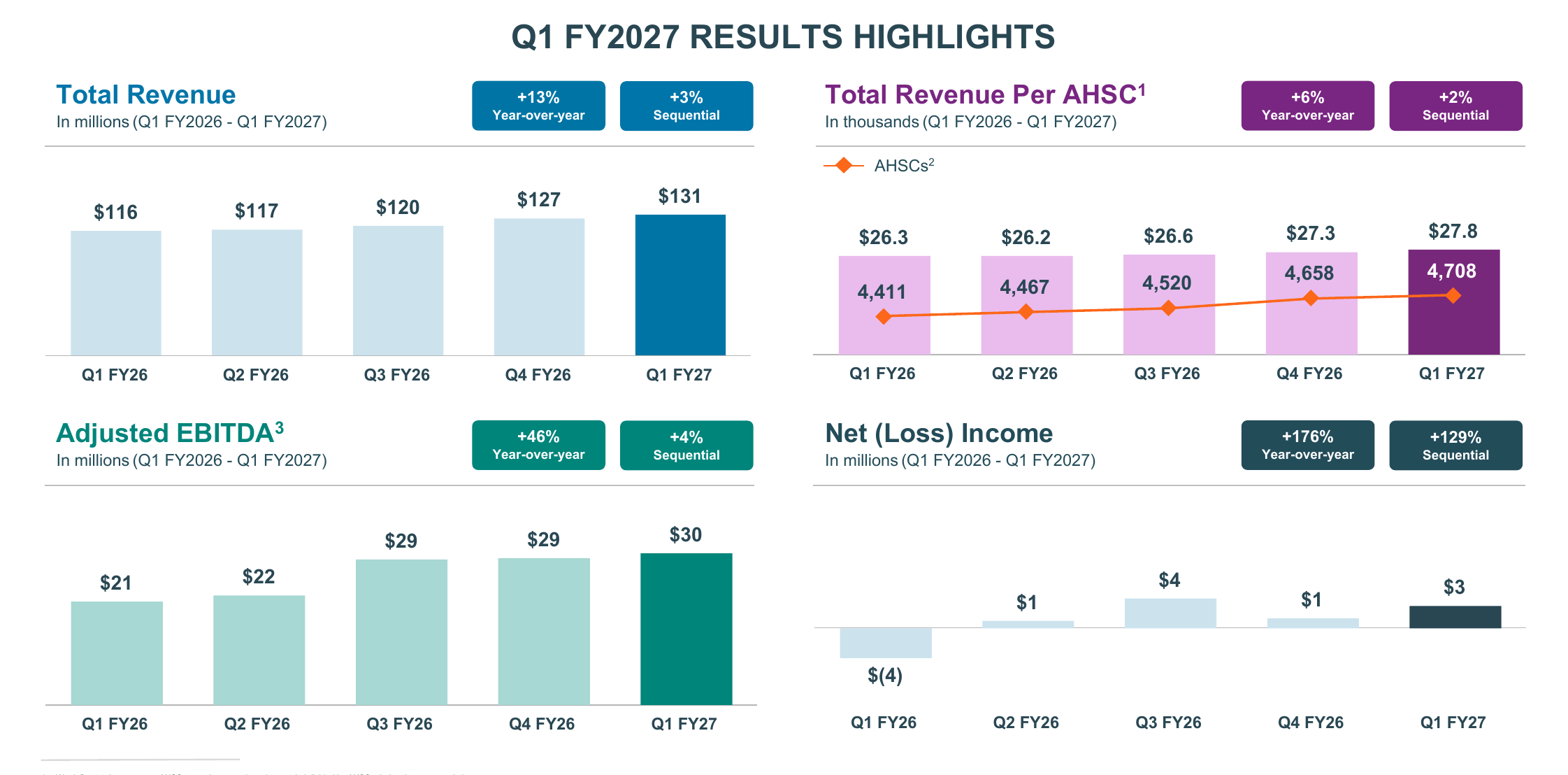

At quarterly cadence, the most recent print (Q1 FY2027) shows the same pattern at higher frequency: +13% year-over-year revenue, rising revenue per client (with AHSCs still grinding higher), and continued adjusted-EBITDA and net-income expansion.

Exhibit 6. Q1 FY2027 results highlights. Source: Phreesia Q1 FY2027 investor presentation (slide 4).

The installed base: a moat made of distribution

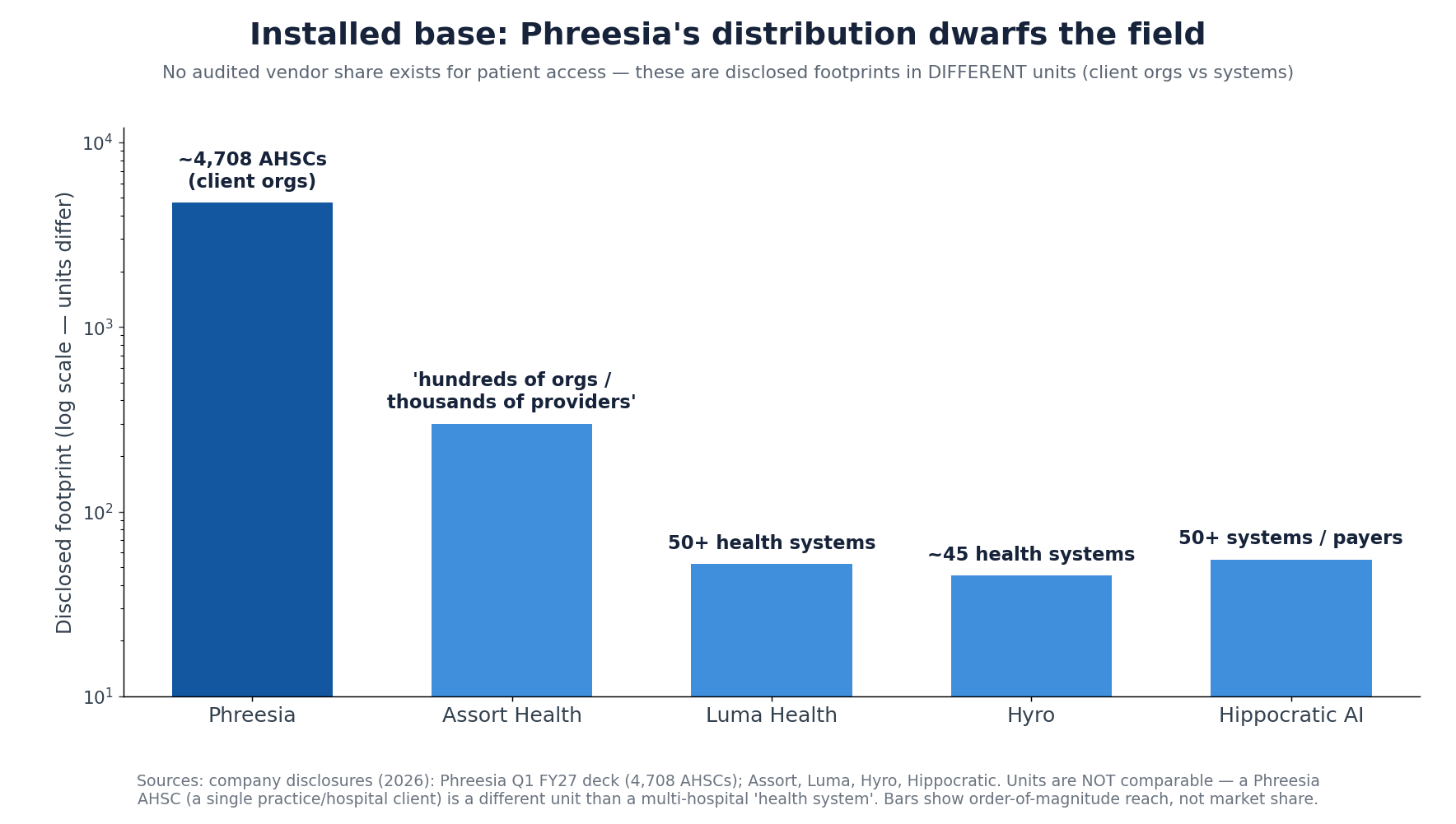

The reason Phreesia matters strategically is the installed base. No audited vendor market-share table exists for patient access, because the category is young and fragmented, so the comparison has to rest on disclosed footprint, and the catch is that the units don’t match. A Phreesia “AHSC” is a single client organization (a practice or a hospital). A startup’s “50+ health systems” can each contain dozens of hospitals. With that warning attached, the order-of-magnitude difference in reach is still the point.

Phreesia’s ideal customer profile spans hospitals, health systems, and, its sweet spot, mid-market ambulatory and specialty group practices that want a single vendor for scheduling, intake, payments and outreach. That’s a broad, shallow footprint: lots of organizations, deep workflow integration, modest revenue per client. The AI-native challengers run the inverse, narrow and deep.

| Vendor | Primary buyer | Disclosed footprint | Latest valuation | Note |

|---|---|---|---|---|

| Phreesia | Ambulatory + health systems | ~4,708 AHSCs · ~180M visits/yr | EV ~$0.64B (public) | Largest installed base; VoiceAI new (Sep 2025) |

| Assort Health | Specialty group practices | ”hundreds of orgs / thousands of providers” · 190M+ voice interactions | $1.2B (Series C, Jun 2026) | Voice-native “Synapse” specialty model; ~$222M raised |

| Luma Health | Health systems + specialty | 50+ health systems | private | KLAS top performer, patient outreach |

| Hyro | Health systems | ~45 large systems | private | Voice + chat; resolves up to ~85% of routine calls |

| Hippocratic AI | Health systems + payers | 50+ systems/payers, 6 countries | $3.5B (Series C, Nov 2025) | More outbound clinical engagement than front-desk access |

The two sides overlap more than the labels suggest. The AI-native challengers, Assort, Luma, Hyro and their peers, also schedule, handle intake, route referrals, take payments, and integrate with the major EHRs. They have those capabilities. They simply haven’t deployed them across a comparable base. The differences that matter are depth and scale. Phreesia’s edge is distribution and breadth: the phone line, intake form, payment page and EHR connections already live inside thousands of organizations, with payments and network monetization layered on top. The challengers’ edge is the technology: voice-native architectures trained on tens of millions of specialty interactions, with deeper autonomous resolution than an intake platform that added a voice agent nine months ago. By reputation the strongest of them are the better voice products (we haven’t independently benchmarked them), and they’re deployed in a fraction of the accounts. One side leads on reach, the other on product.

The product gap may be narrowing

The cleanest version of the strategic case assumes the incumbent can’t build competitive AI itself and therefore has to buy it. Phreesia’s own marketing complicates that assumption. Its VoiceAI page now advertises the kind of metrics that, a year ago, were the AI-native players’ calling card.

Two caveats keep this in proportion. First, these are vendor marketing claims, largely unaudited, and “handled” is a slippery unit. Capturing a message and routing it counts as one thing; genuine autonomous resolution is another, and the headline 80% is drawn from named customer results, not an independently verified average across the base. Second, VoiceAI is young (launched September 2025) and built on top of Phreesia’s existing intake platform rather than as a voice-native model trained on tens of millions of specialty calls, which is still the basis for the voice-native challengers’ claim to deeper, specialty-specific resolution. Without a head-to-head benchmark, “whose agent actually resolves more, on harder calls” is unknowable from the outside.

The direction matters more than the decimal. If even roughly true, Phreesia’s numbers are converging on the category’s best-marketed figures (Hyro cites up to ~85%, and deflection claims across the category cluster in the 70% to 85% range). And Phreesia can switch its agent on across an already-integrated base of 4,700+ organizations in days, a deployment speed a net-new vendor would struggle to match. That cuts two ways. It strengthens the distribution argument: the incumbent can light up modern voice across its base fast, which is what makes the base valuable. It also weakens the cleanest M&A rationale. If Phreesia can build good-enough voice itself, an acquirer’s technology edge shrinks, and Phreesia becomes more able to modernize on its own, or to be the consolidator rather than the consolidated. The product moat the AI-natives are counting on may be narrower, and closing faster, than the funding multiples imply.

The valuation: priced like a tired SaaS company

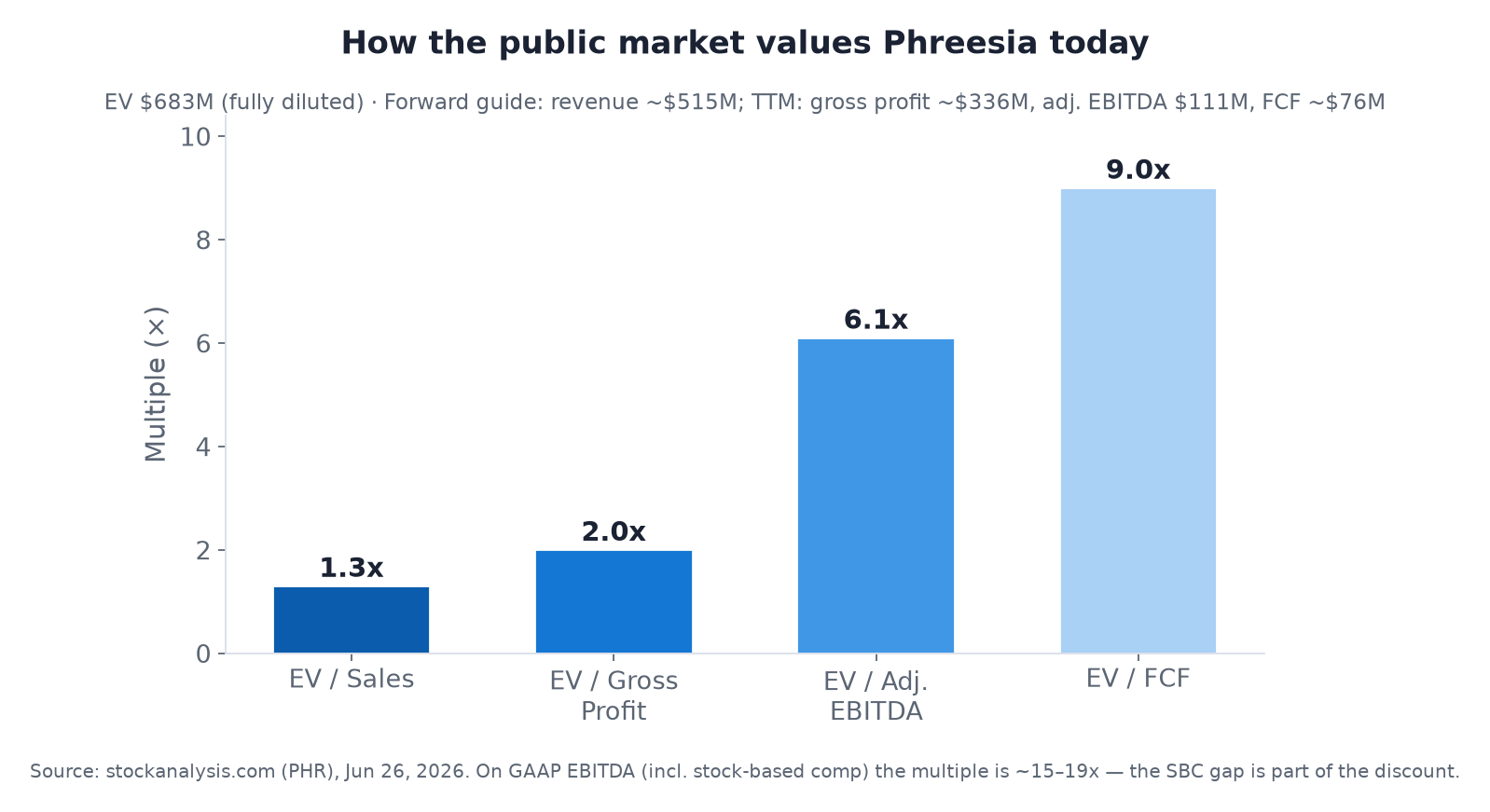

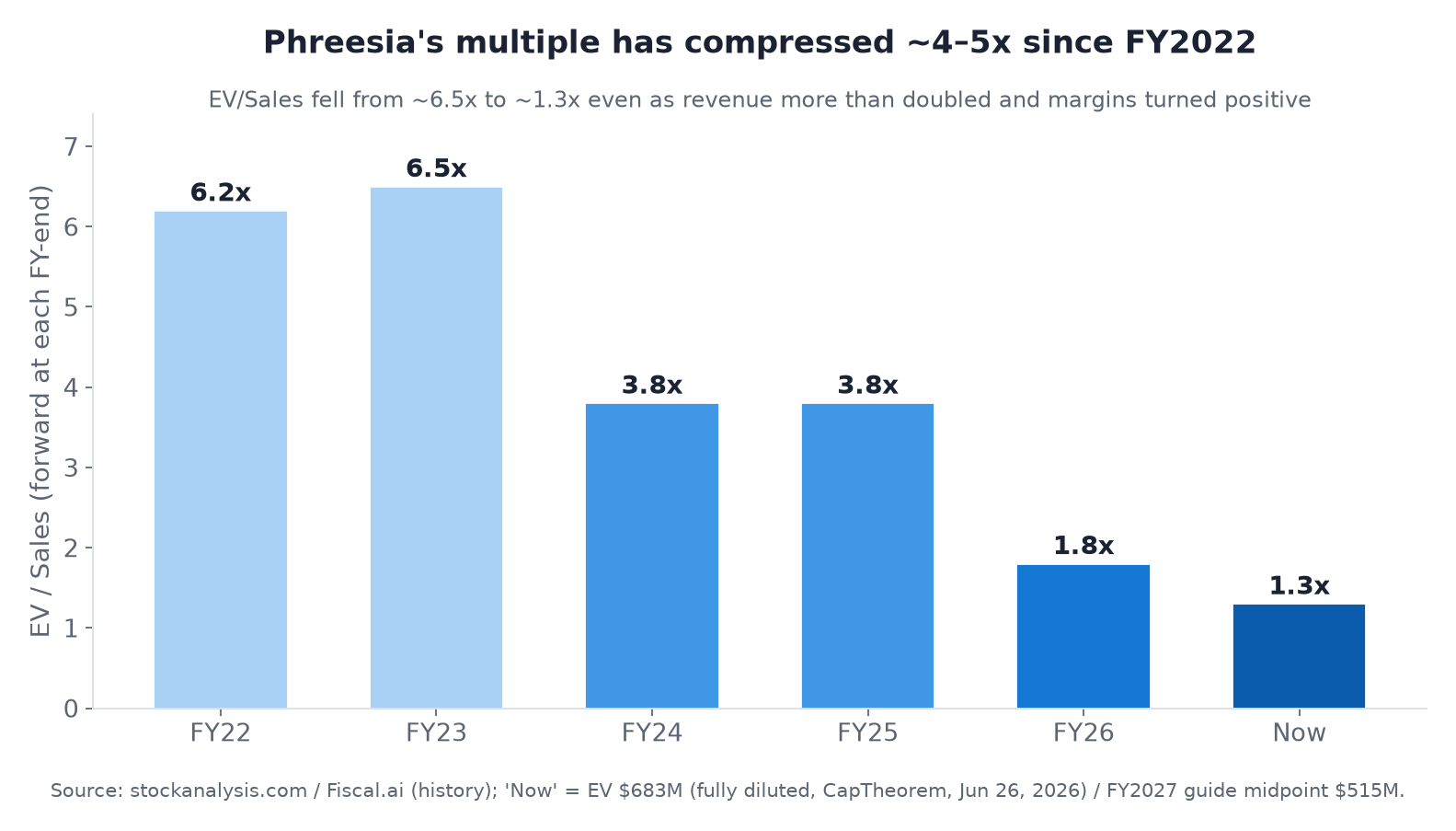

Here is where it gets strange. For all that distribution and the profitability turn, the public market values Phreesia at about ~1.3x forward sales, ~2.0x gross profit, and ~6.1x adjusted EBITDA (EV ~$683M on roughly $515M of FY2027 revenue guidance). Even its EV/FCF is ~9x. These are value-stock multiples, not growth-software multiples.

This is a derating from a much higher starting point. Phreesia traded at ~6.5x sales in FY2023. The multiple has compressed by more than four-fold even as revenue more than doubled and margins flipped positive. That is the textbook fate of a healthcare-IT name whose growth decelerated into an out-of-favor public market.

Why so cheap? Four things stack up. Growth has slowed to single digits and guidance was cut. A chunk of revenue is cyclical, pharma-funded network/ad spend (the source of the cut). The heavy stock-based comp means GAAP EBITDA is a quarter of the “adjusted” figure, so on a GAAP basis the EV/EBITDA multiple is closer to ~15x to ~19x. And the whole public healthcare-IT group has been derated since 2021. (Part of the recent margin expansion also came from a 2026 workforce restructuring, reportedly on the order of ~220 roles, which supports the operating-leverage story and is itself a demand-caution signal alongside the guide cut.) The sell-side has moved in step: Piper Sandler, Wells Fargo and Barclays all downgraded in mid-2026, with price targets cut toward $9 to $16, even as consensus stays a nominal “Buy.” For context, Phreesia’s ~6.1x adjusted-EBITDA multiple sits below the broader healthcare-services median (~11x to 12x in 2026) and its ~1.3x forward sales is at the low end of public health-IT SaaS.

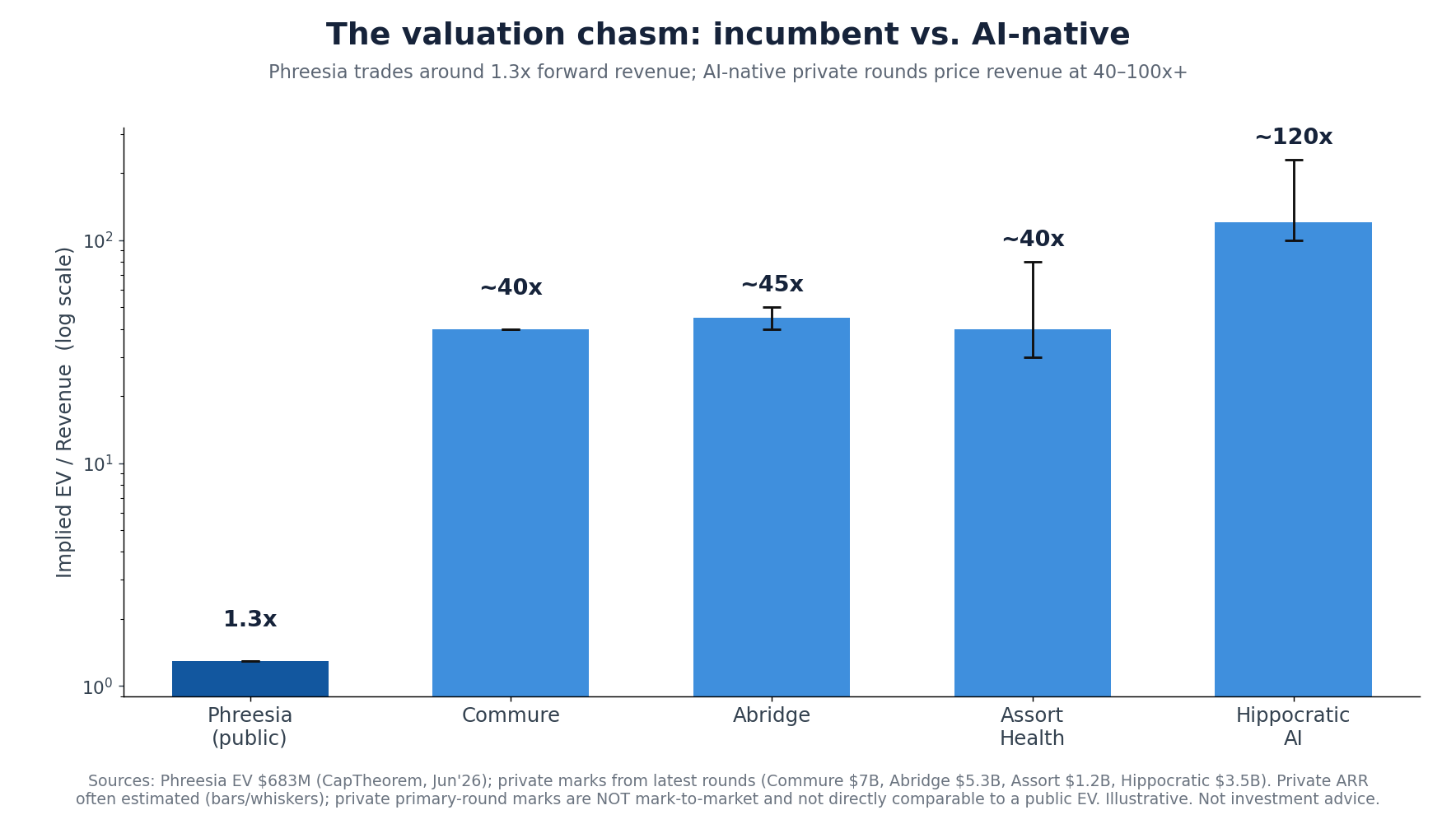

The chasm: 1.3x versus 40 to 100x

Now place the incumbent next to the insurgents. The AI-native patient-access and ambient cohort is being financed at revenue multiples one to two orders of magnitude higher. Abridge raised at $5.3B on roughly $117M of ARR (~45x). Commure sits at a reported $7B on ~$176M (~40x). Hippocratic AI raised at $3.5B on an ARR still in the tens of millions (>100x). And Assort, the most direct patient-access comparable, raised $120M at $1.2B in June 2026; Forbes estimates its annualized revenue is now above $30M (Assort itself discloses only that revenue has grown 20-fold in 15 months), which puts the round around ~40x.

Part of that gap is justified, and part of it is a tale of two markets. The justified part: the startups are growing several-hundred percent a year off small bases, run voice-native rather than retrofitted architectures, and carry optionality the market is happy to underwrite. The two-markets part: private primary-round marks are set by a single lead investor buying a sliver of preferred stock with liquidation preferences, not by a daily auction of the whole company. They are not mark-to-market, and they are not directly comparable to a public EV. The truth sits in between. Even discounting the private marks heavily, the structural pattern holds: the market is paying richly for AI-native growth and steeply discounting incumbent distribution.

Why the incumbents can’t just “go modernize”

The obvious rejoinder is that Phreesia’s customers should simply adopt the better technology. In practice that is exactly what doesn’t happen quickly, and the reason is the buyer.

Phreesia’s base spans hospitals and health systems but leans toward ambulatory and specialty group practices, including many independent practices and the PE-backed platforms rolling them up. As a general tendency, and larger health-system clients are better resourced, so this isn’t universal, many of these organizations are not set up to run a modernization program. They have thin or outsourced IT, limited integration engineering, aging systems of record, and little slack budget or staff to stand up, integrate, security-review and change-manage a new vendor across the front desk. Ripping out an embedded intake/payments/EHR workflow and replacing it with an AI-native stack is a multi-quarter project with real switching costs and real clinical-operations risk. For a 12-provider orthopedic group, that is a heavy lift with a long payback. Even the PE platforms, which do have the sophistication, move deliberately: standardizing one vendor across a portfolio means procurement, security (SOC 2, sometimes HITRUST), integration, and a phased rollout across affiliates. The capability and the appetite to modernize are scarce exactly where Phreesia is strongest.

That inertia is Phreesia’s underappreciated asset, and the insurgents’ real bottleneck. Which leads to the strategic point.

The setup: a classic incumbent-meets-disruptor combination

Read the two sides together and a familiar pattern appears.

On one side, an incumbent with working product and enormous distribution but a decelerating multiple and technology that is unlikely to out-innovate venture-funded, AI-native specialists. Phreesia has the footprint, the integrations, the payments rails, and the customer relationships, assets that took the better part of two decades and hundreds of millions of dollars to assemble, and that the market is currently valuing at barely more than its revenue.

On the other side, AI-native scalers with a leading product but a long, expensive grind ahead to build distribution. The hard, slow, unglamorous work of dislodging incumbents one small clinic at a time, the sales cycles, the implementations, the go-lives, the security reviews, is precisely what venture money is least able to buy quickly. These AI-native players can win logos at impressive rates, yet assembling a 4,700-organization installed base organically would take many years.

That asymmetry is the textbook setup for a strategic combination. The fastest route for an AI-native scaler to acquire distribution is to buy the incumbent, inheriting the footprint, the payments stream, and the EHR integrations at once, then layering its own modern product on top of that base over time. The incumbent’s installed base becomes the disruptor’s distribution; the disruptor’s technology becomes the incumbent’s product roadmap. A public company trading around 1.3x forward sales, with positive free cash flow to help fund the deal, is an unusually affordable way to acquire a head start on two decades of go-to-market.

Who could plausibly do this? A direct “minnow-swallows-whale” acquisition by a single venture-stage startup is a stretch on its own balance sheet. The same logic runs through the better-capitalized strategics and their backers: the General Catalysts, the platform consolidators, and the large ambient players widening into patient access. Any of them could pair AI-native product with Phreesia’s rails. The mechanism doesn’t depend on which entity executes it. Combine working distribution with leading-edge technology, and, executed well, the combined entity can scale faster than either could alone.

If the integration goes right: the value unlock

The risks below are real, and they describe a failure mode. It’s worth working the other scenario just as hard. Assume the acquirer executes: disciplined integration, a credible migration path, customers retained, and the combination is genuinely additive. What does winning look like? Four distinct sources of value stack up.

1. Immediate scale, a decade of distribution. An AI-native scaler is, generously, a low-tens-of-millions-ARR business reaching a few hundred organizations. Phreesia guides ~$515M of FY2027 revenue across ~4,700 client organizations and ~180M patient visits a year. Bolting them together is a step-change in both revenue and reach, the exact footprint that would otherwise take many years and hundreds of millions in sales spend to assemble organically.

2. Cross-sell into a warm base, the revenue synergy. Phreesia’s installed base is the channel every voice-AI startup is trying to build one logo at a time. Phreesia already launched a VoiceAI product (Sep 2025), which means the demand is validated and the integration surface exists, though that product is newer and built on the existing platform rather than voice-native from the ground up (as noted above, its marketed metrics are already competitive). Swap in a leading voice-native engine, or simply scale Phreesia’s own, and you’re upgrading a product to thousands of organizations that already trust the vendor and already route their phones, intake and payments through it. Attaching modern voice to even a modest fraction of 4,700 organizations could be a large, and comparatively fast, ARR layer. And it runs in both directions: the AI-native scaler’s customers gain Phreesia’s payments and network-monetization rails, lifting revenue per client across the combined base (recall Phreesia’s whole model is expanding revenue per AHSC through cross-sell).

3. It can largely fund itself. This is the unusual part. Most “buy-the-incumbent” stories require an acquirer to carry a cash-burning target. Phreesia runs the other way: ~$100M+ of adjusted EBITDA and ~$60M to $75M of free cash flow. For a venture-funded scaler that is otherwise spending to grow, acquiring a profitable, cash-generative base can reduce blended burn and help finance the modernization from the target’s own cash flows. (That cash flow would be partly offset by any debt raised to fund the deal and by integration spend, a financing question a real model would have to work through, not a free lunch.)

4. A re-rating you earn, not buy. The payoff is not arbitraging Phreesia’s multiple at close. Its standalone multiple is probably fair for a single-digit grower with cyclical ad revenue. The combined entity, an AI-native product scaling on Phreesia’s installed base, is a different business than either piece alone, and if it proves that out publicly over 12 to 24 months, the market can re-rate it from “tired health-IT incumbent” toward a growth platform. That re-rating is earned through execution, not assumed in order to fund a deal. Part 2 grounds the range: a credible 4× to 5× revenue multiple on the combined ~$600M of revenue implies ~$2.4B to $3.0B, and a sensible ~16× to 20× EV/EBITDA, in line with quality software and health-IT rather than an AI-native moonshot. Still far above Phreesia’s ~1.3× today, still earned rather than bought, and before counting new voice ARR or cross-sell.

Add a fifth, harder-to-quantify prize: data. Combine the AI-native scaler’s voice-interaction data with Phreesia’s intake, payments and EHR-integration data across ~180M annual visits, and you get a training and product-feedback asset that neither side has alone. It is the kind of proprietary, vertical dataset that compounds an AI product’s advantage over time.

Phreesia as a strategic M&A asset

Step back, and the specific buyer matters less than what Phreesia represents: a strategic asset whose value to an AI-native acquirer is different from, and arguably greater than, its value as a standalone public stock. Four conditions make it attractive: durable distribution, embedded workflow, positive cash flow, and a depressed public multiple decoupled from where private AI value is being created. Those same conditions describe a shelf of other 2010s health-IT incumbents that built rails into thousands of provider organizations and then watched their multiples compress. For a well-funded modernizer, that shelf is a roll-up opportunity: acquire the rails cheaply, layer modern AI-native product on top, harvest the cash flow to fund the next deal, and compound a distribution advantage that is hard to build organically. Phreesia is one of the clearest current examples, among the cheapest large installed bases sitting next to some of the richest pools of AI-native capital.

If an AI-native clinical-voice unicorn actually wanted that asset, the structure of the deal would matter as much as the price. Three broad paths, with very different risk profiles:

| Structure | How it works | What the AI-native gets | Principal tradeoff |

|---|---|---|---|

| Take-private acquisition | A strategic + PE sponsor (or the startup’s own richly valued equity) buys PHR at a premium and delists it | Full control of the base; integrate privately, off the quarterly clock; Phreesia’s cash flow helps service leverage | The check: a venture-stage company can’t fund a ~$1B+ deal alone. It needs a sponsor, debt, or stock the public market would have to honor |

| Reverse merger (“back-door IPO”) | The private unicorn merges into public Phreesia; its holders control the combined public company, which keeps the listing | Distribution and public-market liquidity without a traditional IPO; public stock as future M&A currency | Highly speculative; forces public-company life early and re-prices the private mark against public multiples |

| Partnership / minority stake | A commercial OEM or white-label deal, or a minority investment, instead of a merger | Channel access for a fraction of the capital and risk; optionality | Doesn’t capture the asset; Phreesia keeps the customer and can switch partners |

The table is the summary; three quick reads. Take-private is the cleanest fit for the thesis, and its binding constraint is the check. A venture-stage company can’t fund a billion-dollar-plus deal from its own balance sheet, so this realistically needs a better-capitalized strategic or sponsor, or the acquirer’s own stock credited near its private mark, precisely what’s in doubt. The reverse merger is the most intriguing and the most speculative path: a “back-door IPO” that hands the AI-native company both the installed base and public-market liquidity, in exchange for the quarterly treadmill and a public re-pricing. Part 2 works through its mechanics, math, and precedents in detail. The partnership path reaches the base for a fraction of the capital and risk, and doesn’t capture the asset, because Phreesia keeps the customer and can switch partners.

Whether any of this fits a founding team’s mission, control preferences, and horizon is a genuine question, and for many AI-native founders the answer is simply no. So treat it as a thought experiment about how decoupled the two valuation worlds have become, not a recommendation. The narrower point: once you see Phreesia as a strategic asset rather than a cheap stock, the question shifts from “will it re-rate?” to “to whom, and through what structure, is its distribution worth the most?”

The other side of the argument

A fair analysis has to state why this might not happen, or might not work.

The combination is not free money, and the migration risk is often overstated as a “rip-and-replace.” A practice does not have to tear out Phreesia to adopt an AI-native product. The gentler, more likely path is upgrade-in-place: an acquirer takes over one module first, most obviously swapping its voice engine in for Phreesia’s nascent VoiceAI inside the integration that already exists, proves a higher ROI lift than the standalone product, and then expands ACV and share of workflow account by account. That land-and-expand path lowers switching friction, and it doesn’t erase execution risk. Post-merger integration in healthcare IT is genuinely hard, some customer attrition during any transition is normal, and each expansion has to be earned rather than assumed.

Beyond integration, the price is complicated by mix. Phreesia’s network-solutions line carries high margins and still grows. It rose mid-teens year-over-year in Q1 FY2027 even after the guide-down, so it is genuinely valuable. It is also cyclical, pharma-funded advertising revenue, which the market typically capitalizes at a lower multiple than recurring software. An acquirer focused on the AI-native access product might value the business on a sum-of-the-parts basis and apply a more conservative multiple to that slice, which muddies a clean headline price (a valuation-modeling question beyond this article’s scope). And Phreesia is not a passive target. It is profitable, cash-generative, and could simply keep harvesting its base, build its own AI capability (its VoiceAI already markets ~80% call resolution and five-day deployment), or argue that it is the natural consolidator of patient access rather than the consolidated. The most important risk to the entire thesis may be the EHR vendors, which loom over the whole landscape. Epic, athenahealth and Oracle keep bundling more of the front office (scheduling, intake, increasingly voice) into the system of record, often at no incremental cost. A good-enough native option shipped inside the EHR could compress the value of both the incumbent’s rails and the insurgents’ point products at once. That is perhaps the strongest argument against treating distribution as a durable, scarce moat. The valuation gap is real; whether it closes through M&A, through Phreesia re-rating on its own execution, or not at all, is genuinely uncertain. (Part 2 develops this counter-case further: why, in a large and growing non-zero-sum market, the combination’s value rests on execution and a durable product edge rather than on out-maneuvering anyone.)

Issues for further diligence

Three things that bear on the thesis deserve more rigor than a primer can give them. They are flagged here with a first read, the kind of company-specific diligence a serious acquirer (or skeptic) would underwrite before acting, distinct from the strategic and economic deep-dive in Part 2.

Stock-based compensation: a drag, but a restructurable one. Phreesia’s ~$68M of annual stock-based comp (~14% of revenue) is the main reason GAAP EBITDA (~$25M) is so far below the “adjusted” figure ($101.5M), and it is a genuine economic cost. Two nuances matter for an M&A lens. First, the market capitalization and enterprise value used here are computed on shares already outstanding, and the company’s diluted share count already absorbs in-the-money options and RSUs, so a good chunk of past SBC is reflected in the valuation. The incremental drag is mostly future grants and the GAAP earnings optics, not a hidden liability on top of EV. Second, SBC is one of the most restructurable costs in an acquisition: target equity awards are typically converted, cashed out, or replaced with the acquirer’s compensation structure, so the standalone SBC trajectory is not destiny. A proper treatment would rebuild EV on a fully-diluted, treasury-method basis and model the post-deal comp structure, which is out of scope here.

The securities litigation: early-stage and unproven. Following the March 30, 2026 guidance cut and ~27% drop, Phreesia drew a federal securities class action (class period May 8, 2025 to March 30, 2026) alleging the company overstated the durability of pharma marketing commitments in Network Solutions and the reliability of its FY2027 guidance. As of this writing it is at the lead-plaintiff stage (deadline July 13, 2026), before any motion-to-dismiss ruling, with the allegations unproven. This is the common pattern of a “stock-drop” suit filed by plaintiff firms after a sharp decline; many such cases are dismissed or settled modestly, and a meaningful minority survive, and the merits here turn on a fact question, what management knew, and when, about the pharma softness, that only discovery can resolve. It is a real diligence item and a potential cost/contingency, not a settled liability; sizing it is out of scope here.

Governance, management and shareholder dynamics: receptive, on the surface. Phreesia is founder-led (CEO Chaim Indig, co-founder, since 2005) though not founder-controlled: insiders hold roughly 5% while institutions hold ~99% (Vanguard and BlackRock among the largest), and the board is moving toward an independent chair (Ramin Sayar) and a smaller, refreshed slate after the June 2026 annual meeting. A widely-held, institutionally-owned company with low insider ownership and independent governance is, in the abstract, more receptive to a credible premium bid than a founder-supervoting structure would be, though confirming the share structure, change-of- control provisions, recent insider selling, and any takeover defenses is exactly the kind of work a follow-up should do before drawing conclusions.

None of these changes the core argument. The valuation gap and the strategic logic stand on their own. Each is a live question a serious acquirer (or a serious skeptic) would underwrite before acting.

The takeaway

Strip it down and the situation is simple. The public market is pricing Phreesia as a no-growth, out-of-favor health-IT name, about 1.3x forward sales, while the private market pays 40 to 100x revenue for AI-native companies chasing the same buyers with better technology and a fraction of the reach. Distribution and technology have been decoupled in price. That decoupling looks unstable. One of the cheapest large installed bases in patient-facing healthcare software is sitting next to a cohort of richly funded scalers that would benefit enormously from that distribution and would take years to build it themselves. Whether or not anyone acts on it, the gap, and the reason the incumbent’s “modernize on your own” path is blocked for the very customers it serves, is the thing to watch. Price it wrong in either direction and you misjudge both the stock and the startups chasing it.

Sources & method

The Phreesia enterprise value used throughout this piece is a fully-diluted figure (it adds the antidilutive option/RSU overhang to the share count, then nets debt), which runs a little higher than the basic-share EV some data providers quote.

| Phreesia (NYSE: PHR) | Phreesia enterprise value (author’s calculation, as of 6/26/2026) |

|---|---|

| Basic market cap | $622M |

| Fully-diluted shares | 66.01M |

| FD market cap | $665M (+6.9%) |

| Enterprise value | $683M |

Primary disclosures and market data are point-in-time (late June 2026).

Phreesia: financials, guidance, product

- Q1 FY2027 investor presentation & shareholder letter (segment revenue, AHSCs, revenue-per-AHSC, adjusted EBITDA, opex ratios, free cash flow, FY2027 guidance): https://s24.q4cdn.com/837435241/files/doc_financials/2027/q1/Q1-FY27-IR-Presentation.pdf

- Q1 FY2027 earnings-call transcript: https://www.fool.com/earnings/call-transcripts/2026/05/27/phreesia-phr-q1-2027-earnings-transcript/

- SEC filings (FY2026 8-K / income statement); revenue, margins & trading data as of the Jun 26 2026 close: stockanalysis.com · Fiscal.ai

- FY2027 guidance & sell-side actions: Seeking Alpha · TheFly

- VoiceAI product claims (~80% call resolution, five-day deployment), vendor-stated marketing, captured June 2026: https://www.phreesia.com/products/phreesia-voiceai/

Private-peer valuations & ARR (primary-round marks, not mark-to-market, and not directly comparable to a public EV)

- Assort Health, $1.2B Series C (Menlo, Jun 2026); annualized revenue above $30M and “20× in 15 months,” per Forbes (Amy Feldman, Jun 24 2026): https://www.prnewswire.com/news-releases/assort-health-raises-120-million-series-c-to-scale-largest-deployment-of-ai-agents-for-the-patient-journey-302808634.html · also TechCrunch / HIT Consultant

- Abridge, $5.3B, ~$117M ARR: https://techcrunch.com/2025/06/24/in-just-4-months-ai-medical-scribe-abridge-doubles-valuation-to-5-3b/ · https://sacra.com/c/abridge/

- Hippocratic AI, $3.5B Series C: https://hippocraticai.com/hippocratic-ai-announces-series-c-funding-126-million/

- Commure, $7B: https://www.modernhealthcare.com/health-tech/mh-commure-financing-valuation-general-catalyst/

Comps, market sizing, legal & governance

- Public health-IT comps (Definitive Healthcare, GoodRx) & sector EV/EBITDA multiples: https://stockanalysis.com/stocks/dh/statistics/ · https://focusbankers.com/healthcare-ebitda-multiples/

- Patient-access market sizing: Grand View Research · Towards Healthcare

- Securities class action, plaintiff-firm filings (Faruqi & Faruqi; Levi & Korsinsky) & reporting

- Ownership, board & management: Phreesia proxy (DEF 14A) · stockanalysis.com · Simply Wall St

Company-level receipts and links are maintained separately. Figures are point-in-time and directional; private-round valuations are not mark-to-market and not directly comparable to a public enterprise value. This is analysis, not investment advice.