Private equity's AI underwriting & deployment gap: GTM playbook for AI-native Scalers

Private equity committed to AI faster than it can use it. Only about a fifth of portfolio companies have a use case in production, and deal teams are short on AI to underwrite with. For AI-native scalers, the space between underwriting and deployment is a distribution channel. The door most vendors walk through is the one that pays least.

Private equity’s rush into AI

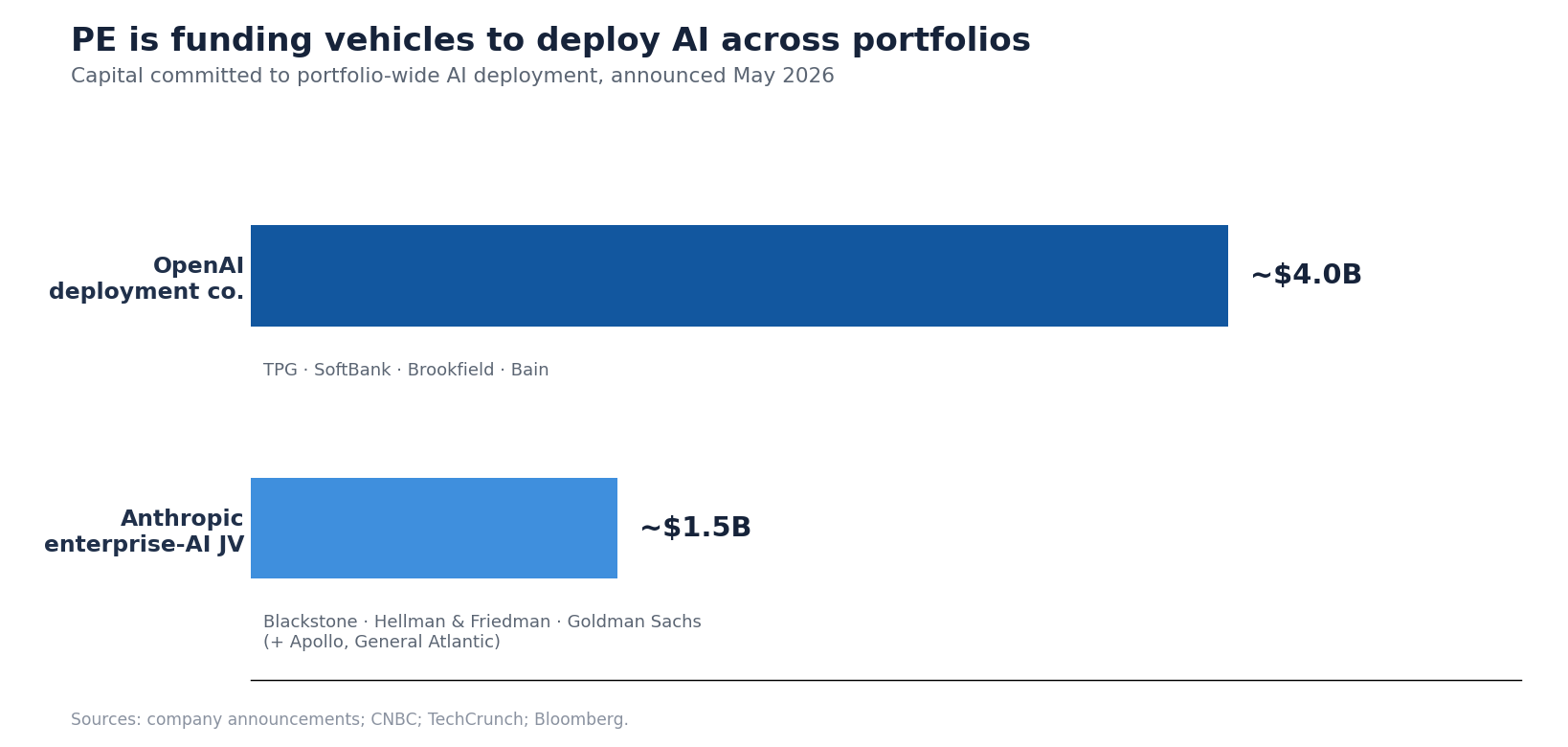

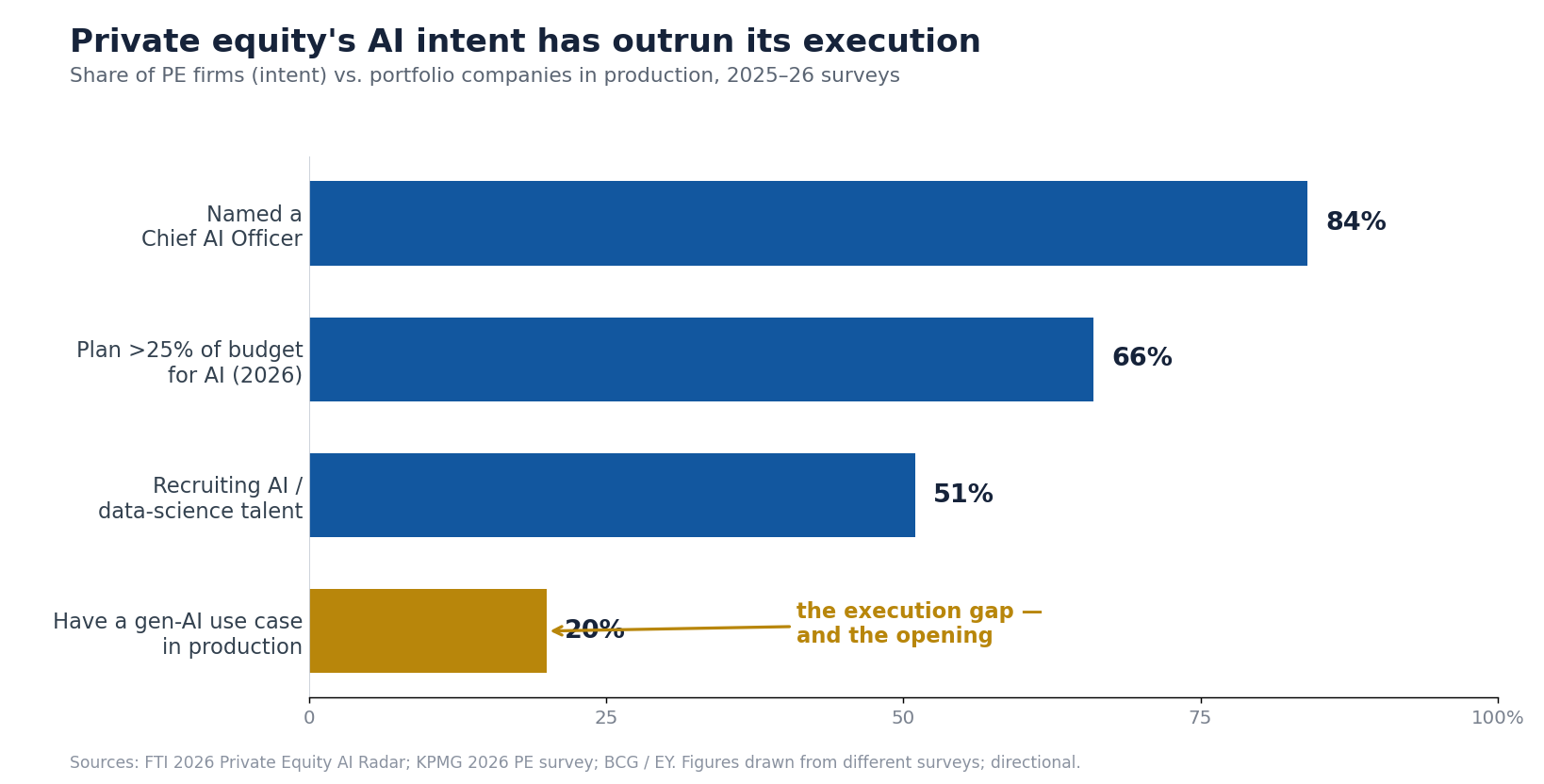

By 2026, two-thirds of private-equity firms expect to put more than a quarter of their budget into AI, and 84% have named a chief AI officer. The biggest firms are building deployment vehicles with the AI labs directly. Anthropic has a roughly $1.5B venture with Blackstone, Hellman & Friedman, and Goldman Sachs to push Claude across their portfolio companies, and a parallel OpenAI vehicle is backed by TPG, SoftBank, Brookfield, and Bain. Independent deployment partners are springing up around the same gap. Tenex.co positions itself as an AI-transformation partner that sets and executes enterprise AI strategy. Invisible Technologies has a private-equity offering for diligence, fund operations, and FP&A workflows. Tribe AI describes work with leading PE firms and their portfolio companies, and Distyl AI packages forward-deployed engineering and operating-model transformation for large enterprises. Hebbia and AlphaSense sit one layer removed. They scale AI into banking, investing, and market-intelligence workflows, with vertical portco deployment a secondary concern.

Intent has outrun execution

For all that spending, little of it is live. Recent surveys put only about a fifth of portfolio companies with a single generative-AI use case in production, and the deal teams doing the buying are just as short on AI to underwrite with. The reason is mundane. Wanting AI and having the engineers to build and deploy it are different things. Most firms, and most of their portfolio companies, have the first but not the second. For an AI-native company, that gap between intent and capability is a distribution channel.

Make the sponsor the channel

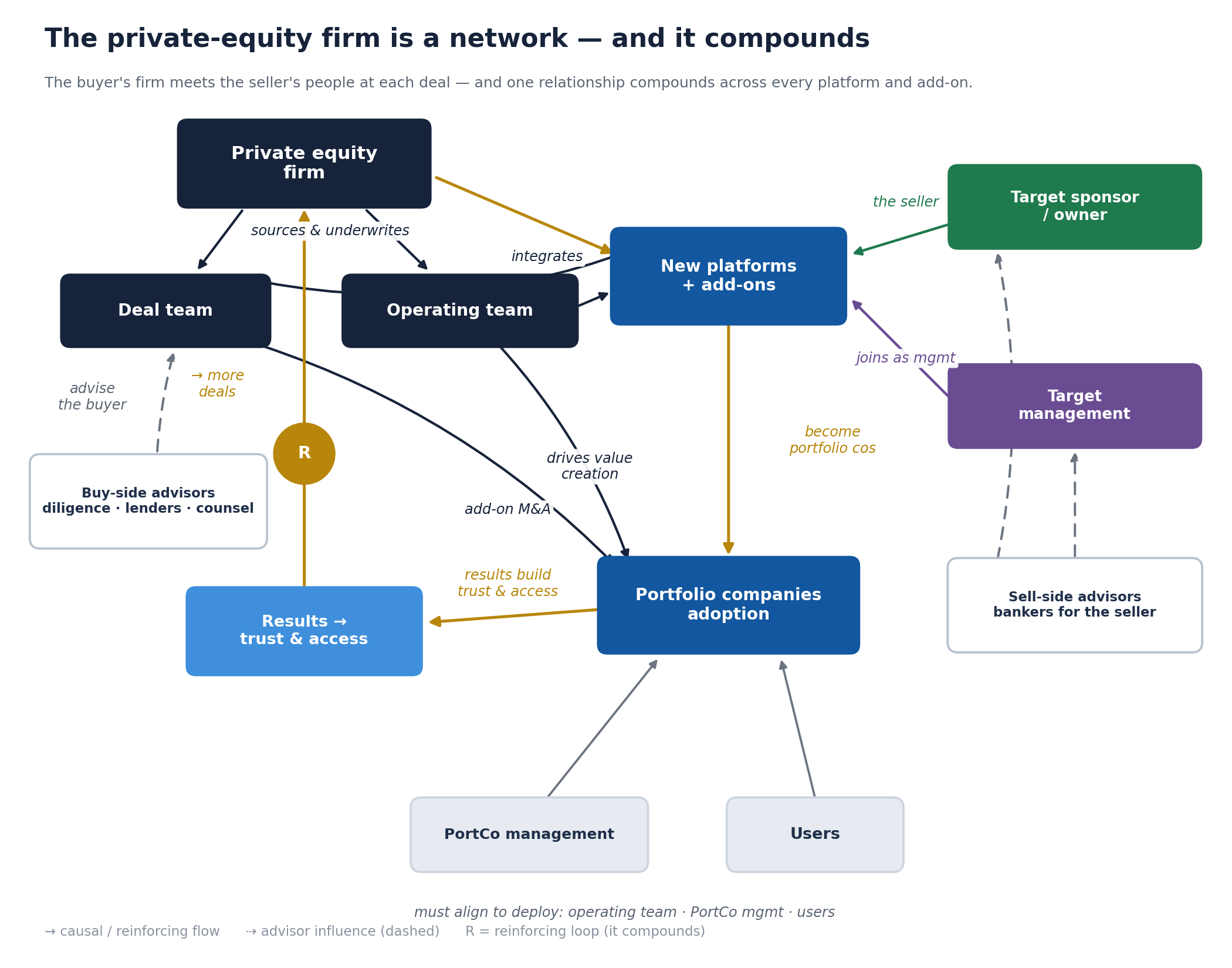

Selling into one portfolio company at a time, then hoping for referrals, is table stakes. Every vendor eventually runs that motion. It is slow, and it is crowded. The real leverage is to treat the sponsor itself as the channel, because a sponsor is two things a single customer is not: an engine and a network.

The engine is that a sponsor keeps buying: a stream of new platforms and a steadier stream of add-on acquisitions, each one another company to serve. Land inside one portfolio company and prove it out, and the relationship compounds. Every deployment builds the results and the trust that earn access to the next deal. One sponsor relationship is worth far more than one sale.

The network is that there is no single buyer, and it runs wider than the fund. A product that touches the business has to win the deal team, the operating (value-creation) team, portfolio-company management, and the users who actually adopt it. A yes from one still leaves the rest to win. It runs wider still: buy-side advisors run diligence for the firm, and sell-side bankers represent the target across the table. Both sit in the deal flow early, before anyone is fielding a software pitch.

So the sharper question is where you enter that network, to whom, and what you bring.

What deal teams need, and what AI-native teams can build

PE deal and operating teams are short on three things. They need time to reach conviction on a target under competitive pressure. They need a read on whether its technology and operations can carry the thesis. And after close, they need the capacity to execute the value-creation plan they underwrote. Consultancies fill some of this with people and templates, slowly and at cost. An AI-native team brings a different asset. It can build. The same engineering and proprietary data that power its product convert, fast, into what a deal team wants at underwriting: benchmarks from real operating data, quick technical and operational reads, agentic analysis that compresses weeks into days. After close, they convert into the deployment capacity the portfolio is missing.

Where the leverage actually is

Built deliberately, those capabilities are more than marketing. They are entry points, and the earliest ones are the most valuable. The crowded door is the post-close pitch to a portfolio company. The higher-velocity wedge is to enter in the deal process itself, where a fast, credible, vertical-AI read helps a deal team win and de-risk the deal. Earn trust there and it carries through diligence into deployment, then compounds across the portfolio. A cold post-close pitch never buys that access. Which problems to solve, for whom, in what order, and how each compounds into a portfolio-wide relationship is the substance of the playbook.

Healthcare services private equity, as an example

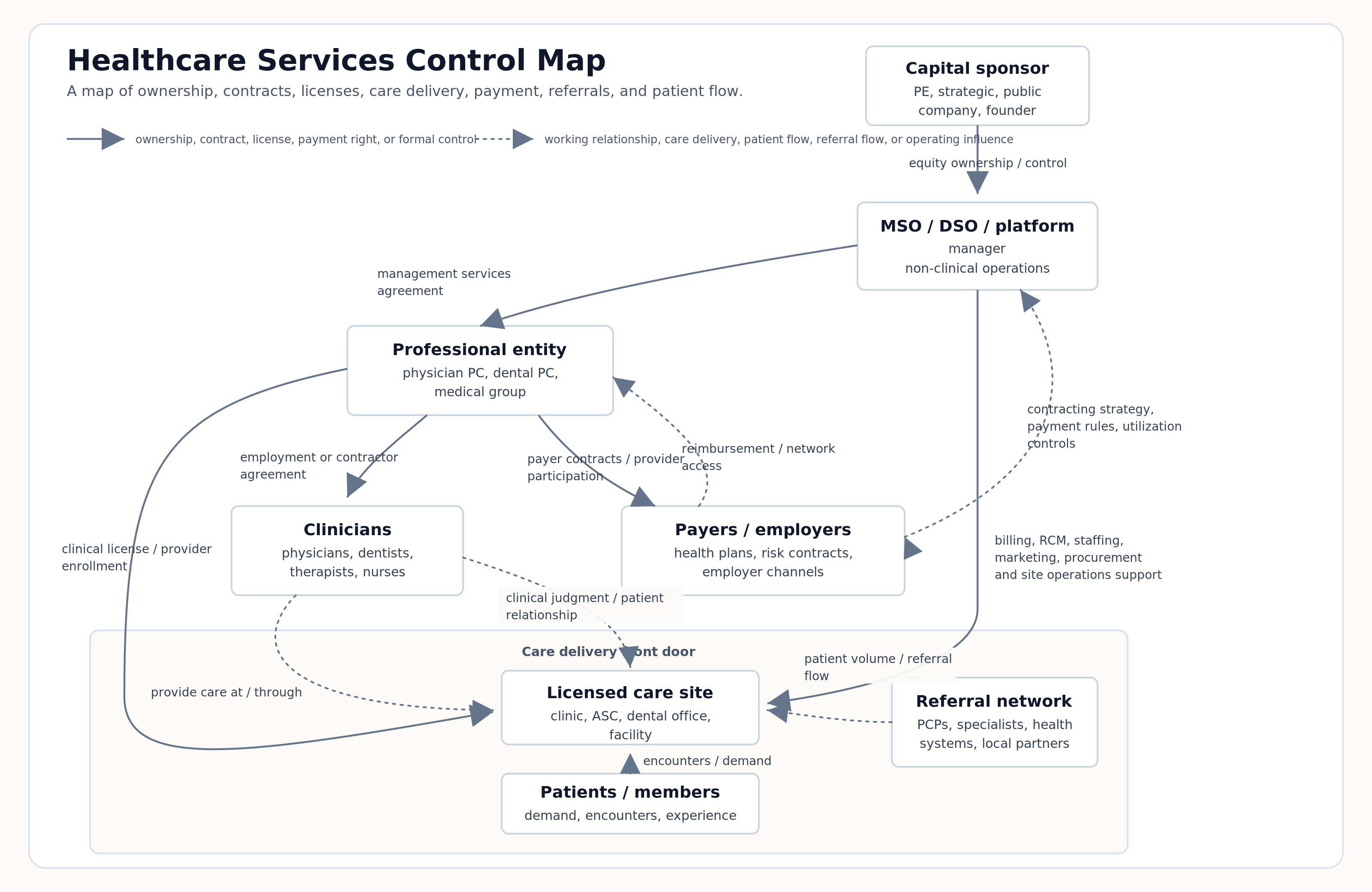

Take healthcare services. It is one of the most active private-equity verticals, and one where the channel’s complexity is easy to underestimate.

There is rarely a single buyer. In a sponsor-owned healthcare business, ownership, the clinical license, non-clinical operations, payer contracts, and referral flow sit in different entities, each with its own decision-maker: the capital sponsor, the management-services layer (the MSO or DSO), the professional entity that holds the license, the clinicians, the payers, and the referral network. A product that touches the front door has to earn buy-in across several of these layers at once. Assume one buyer and the strategy stalls.

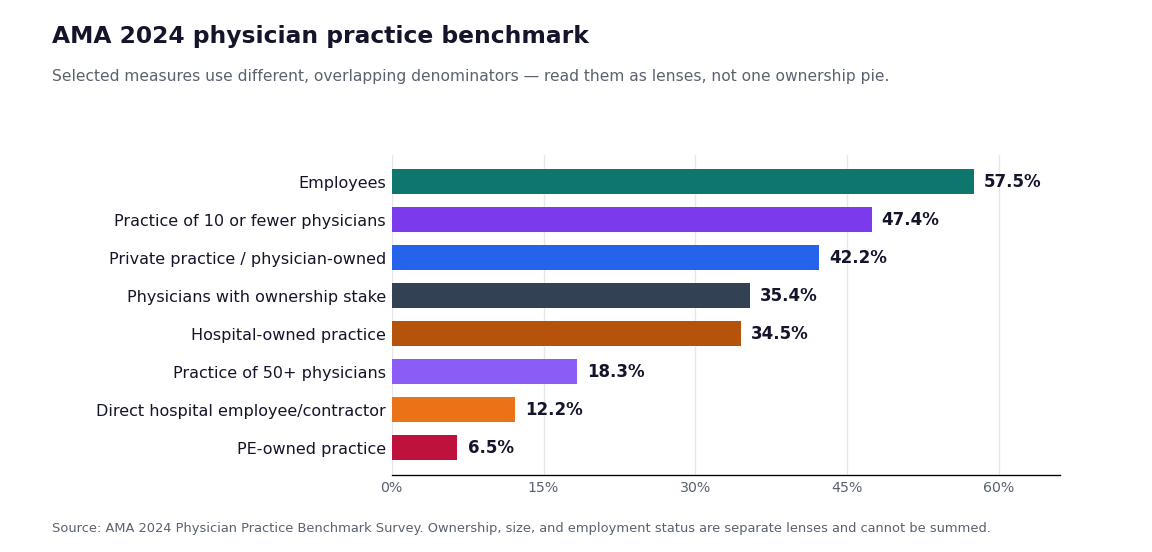

The market is far larger than the portfolios sponsors already own. Only about 6.5% of U.S. physicians practice in a PE-owned group, while roughly 42% remain in independent, physician-owned practices. Sell only into existing portfolios and you chase the smallest slice. The larger opportunity is to meet sponsors where they are expanding, in the continuous flow of new platforms and add-on acquisitions they underwrite out of that independent pool.

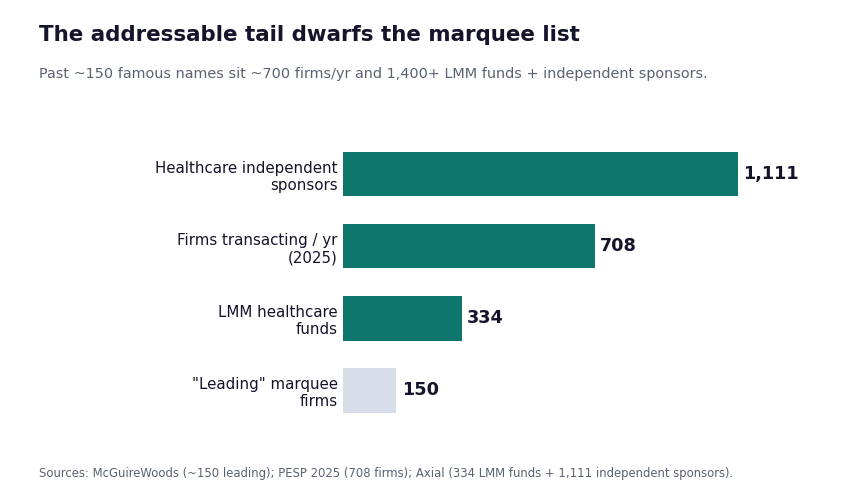

And “the sponsor” is not a handful of megafunds. Past the roughly 150 marquee names sit some 700 firms transacting in U.S. healthcare each year and more than 1,400 lower-middle-market funds and independent sponsors. These are nimble, higher-volume, and largely underserved by the incumbent advisors built for the large-cap tier. A channel that matters has to reach that long tail, well past the brand names.

Those are the structural realities any healthcare PE channel has to navigate: many decision-makers, a market mostly outside existing portfolios, and a long tail of funds. The playbook turns them into a specific motion.

The full playbook

This is the shape of the opportunity, and the map is the playbook itself. That playbook rests on practice rather than theory, built on more than a decade underwriting and executing private-equity deals, plus firsthand operator experience running the transformations these plans call for, and on what it takes to win buy-in at every level: deal teams, operating partners, and the portfolio-company managers who have to live with the result. If you want the detailed version, the specific entry points, the problems worth building for, the sequence, and the economics, reach out for the full PE Strategic Channel GTM Playbook, tailored to your business.

Sources

- FTI Consulting, 2026 Private Equity AI Radar (AI budgets; chief AI officers): https://www.fticonsulting.com/insights/reports/2026-private-equity-ai-radar

- BCG, Inside the AI-First Private Equity Firm (deploy/reshape/invent; production gap): https://www.bcg.com/publications/2026/inside-the-ai-first-private-equity-firm

- EY, US private equity AI insights: https://www.ey.com/en_us/insights/private-equity/us-private-equity-ai-insights

- KPMG 2026 PE survey (AI/data-science recruiting)

- Anthropic × Blackstone, Hellman & Friedman, Goldman Sachs enterprise-AI JV (~$1.5B): https://www.blackstone.com/news/press/anthropic-partners-with-blackstone-hellman-friedman-and-goldman-sachs-to-launch-enterprise-ai-services-firm/ · https://www.cnbc.com/2026/05/04/anthropic-goldman-blackstone-ai-venture.html

- OpenAI & Anthropic enterprise-AI deployment ventures (TechCrunch): https://techcrunch.com/2026/05/04/anthropic-and-openai-are-both-launching-joint-ventures-for-enterprise-ai-services/

- AI-native transformation / deployment examples: Tenex.co AI transformation: https://www.tenex.co/ai-transformation · Invisible Technologies private-equity offering: https://invisibletech.ai/industries/private-equity · Tribe AI enterprise and PE portfolio implementation: https://www.tribe.ai/applied-ai/tribe-2024-wrapped-unlocking-enterprise-ai-at-scale and https://www.tribe.ai/applied-ai/ai-talent-misconceptions-operating-partners · Distyl AI funding / operating-model announcement: https://www.hpcwire.com/bigdatawire/this-just-in/distyl-ai-gains-175m-funding-to-expand-ai-native-operating-model-across-industries/ · Hebbia finance AI platform: https://www.hebbia.com/ · AlphaSense funding and market-intelligence workflow announcement: https://www.alpha-sense.com/press/alphasense-raises-350m-at-7-5b-valuation-and-surpasses-600m-in-annual-recurring-revenue/

Figures are point-in-time and drawn from 2025-26 industry surveys and company announcements; directional. Not investment or legal advice.