Healthcare voice AI isn't one market: a map of who the AI talks to

Microsoft, Abridge, Ambience, Suki, Assort Health, Hippocratic, Commure, Infinitus and the rest get lumped together as 'healthcare voice AI.' They're three different businesses, with different buyers, different moats, and different exposure to EHR bundling. This is a field map of the ambient and voice-agent landscape in 2026, sorted by who the AI talks to.

How to read this. This is a landscape map as of mid-2026, updated in early July 2026. Funding and customer counts in this space move monthly, so treat the numbers as directional and the structure as the point.

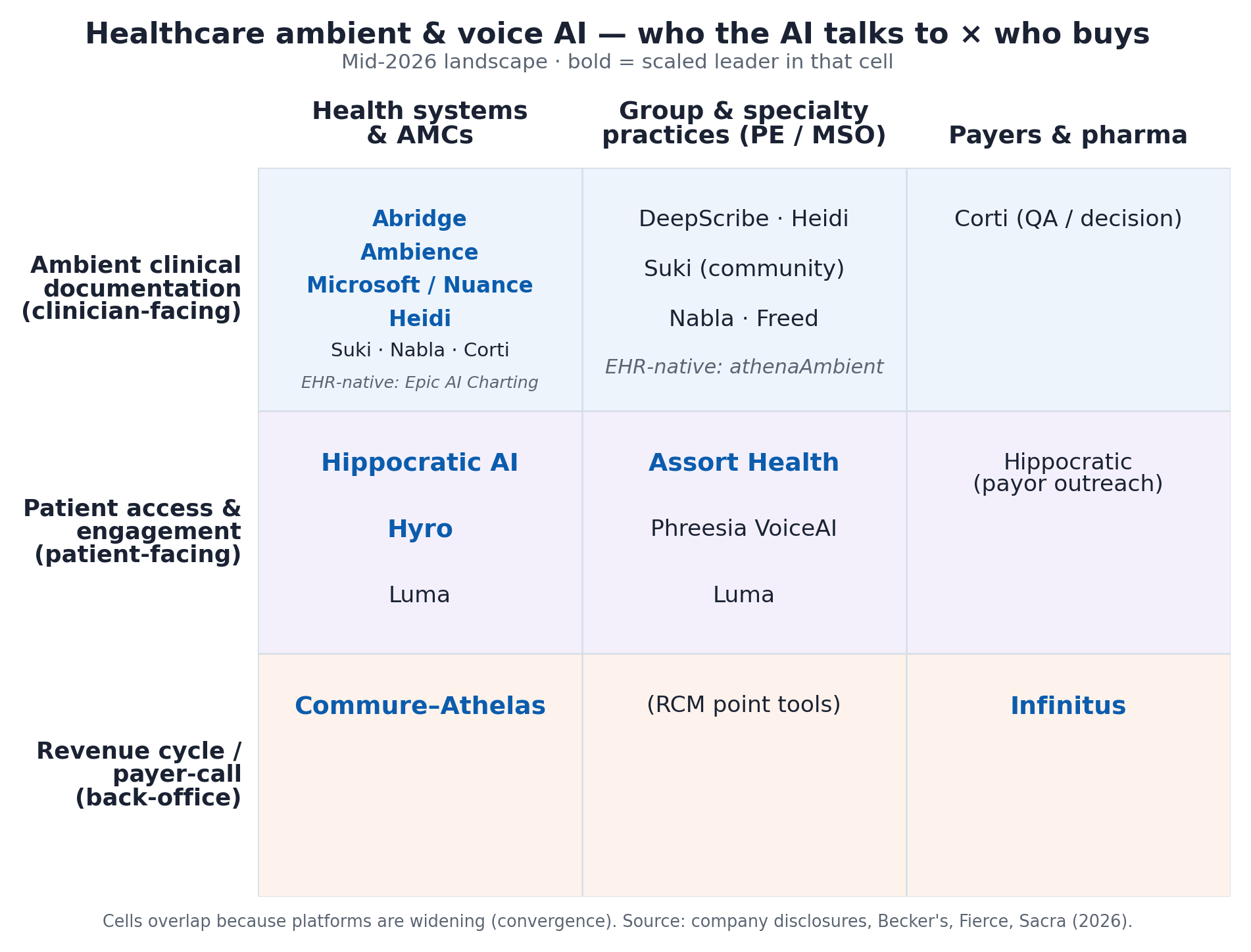

“Healthcare voice AI” is one phrase for a market that’s actually three. A dozen well-funded companies (Microsoft, Abridge, Ambience, Suki, Nabla, Assort Health, Hippocratic AI, Hyro, Commure, Infinitus, and more) get filed under one banner as if they compete. Most of them barely touch the same buyer. The question worth asking is who the AI talks to. That one fact sets the buyer, the data moat, and how exposed a company is to the biggest force in the market: the EHR vendors bundling AI for free.

Two questions place any company

Start with whom the AI interacts with. The clinician (ambient documentation, the scribe), the patient (access and engagement, the front desk), or the payer and back office (revenue cycle: claims, prior auth, benefits).

Then ask who buys it. An enterprise health system, a group or specialty practice (increasingly owned by a private-equity-backed management services organization), or a payer/pharma.

Cross those two and the field sorts itself out.

The three businesses

Ambient clinical documentation sits with the clinician, listens to the visit, and writes the note and the codes. This is the most crowded and best-capitalized lane. Microsoft (Nuance Dragon/DAX), Abridge, Ambience, Suki, Nabla, Corti, and Heidi all compete here. Heidi leads globally by volume, at about 2.4M consults a week across 116 countries, and now rolls out to all Beth Israel Lahey physicians. Abridge is deployed across 150+ health systems and raised to a reported $5.3B valuation. Ambience added a $243M round to push from scribing into coding and clinical documentation integrity. The EHR vendors have now entered too (see below).

Patient access and engagement is a different job. Here the AI talks to the patient and handles the inbound and outbound calls: scheduling, intake, triage, refills, referrals, reminders, post-discharge follow-up. The players split by buyer. Hippocratic AI runs patient-facing clinical agents for large systems and payors. Hyro and Luma sell to health systems. Assort Health and Phreesia’s VoiceAI serve specialty group practices. The moat here is owning the phone channel and the practice’s front-desk workflow, and that neat split by buyer is already starting to blur.

Revenue cycle and payer-call automation is the back office: Commure-Athelas (RCM at health-system scale, reportedly automating 85%+ of revenue-cycle work) and Infinitus (voice agents that call payers for benefit verification and prior authorization). This layer is the stickiest and the least exposed to the disruption below.

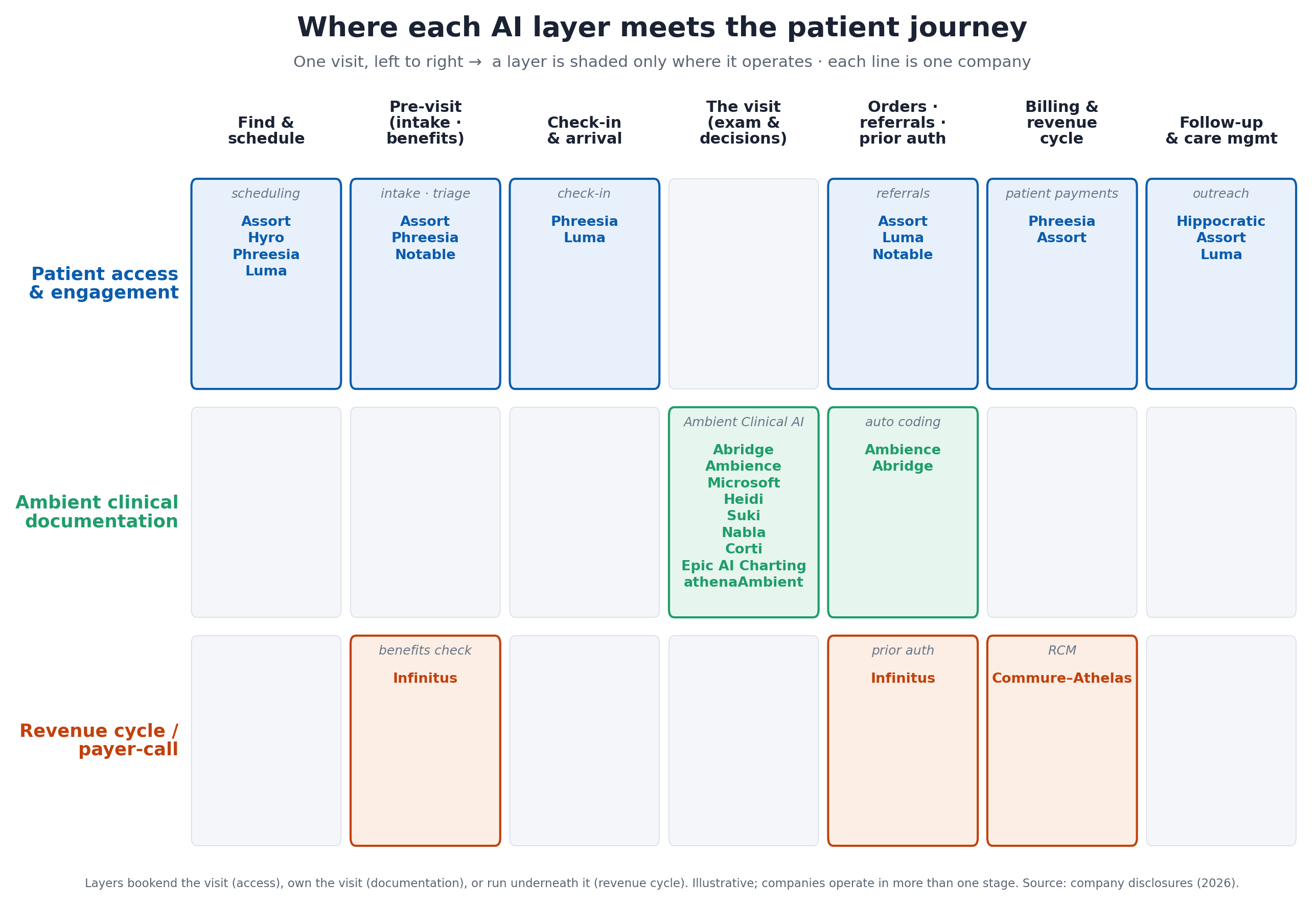

Map it to the patient journey

Follow a single visit from booking to follow-up and it becomes obvious why these layers rarely compete. Patient-access agents bookend the encounter, scheduling and intake before, outreach after. Ambient documentation owns the encounter itself. Revenue-cycle and payer-call automation run underneath the whole thing, from the pre-visit benefits check to the final claim. Different companies, different moments, one patient.

The skeleton is the same everywhere. The mix of layers shifts with how complex the care is and who owns the practice. Three settings show the range:

| Journey stage | Primary care (PCP) | Specialty practice (often PE/MSO) | Hospital / health system |

|---|---|---|---|

| Find & schedule | Patient books an annual physical or sick visit by phone/portal; an access agent routes and books it | A specialty complaint such as knee or back pain; specialty-specific triage routes and books the right appointment | ED arrival or a referral; enterprise central scheduling and registration (e.g. Hyro) |

| Pre-visit | Reminders, medication list, insurance eligibility | Imaging often needs prior authorization (MRI) before the visit: benefits and auth (e.g. Infinitus) | Pre-registration and insurance verification at scale |

| The visit | PCP exam; ambient scribe drafts the note | Surgeon consult and imaging review; ambient note plus specialty coding | Inpatient/ED encounter; ambient documentation including nurses (e.g. Dragon Copilot) |

| Orders, referrals, prior auth | Labs, e-prescriptions, referral to a specialist | MRI/PT orders, surgery scheduling, device prior auth; auth volume is high | Consults and procedures; prior auth at enterprise volume |

| Billing & revenue cycle | A routine claim and copay | A high-dollar surgical claim with device/implant coding | Enterprise RCM across many service lines (e.g. Commure-Athelas) |

| Follow-up & care mgmt | Chronic-care outreach, refill management | Post-op recovery calls and PT-adherence nudges | Post-discharge engagement to reduce readmissions (e.g. Hippocratic AI) |

Read across the rows and the strategic picture falls out. Primary care runs high-volume and low-complexity, so access and documentation dominate and EHR-native scribes bite hardest here. Specialty practices like orthopedics carry heavy prior-authorization and surgical-RCM loads, run on specialty-specific workflows, and increasingly get bought through a single PE/MSO platform, which leaves patient-access and payer-call automation a lot of room. Hospitals light up every layer at once: enterprise documentation (now extending to nurses), enterprise revenue cycle, and post-discharge engagement to keep patients from coming back.

Same label, completely different businesses

Pick any two companies filed under “healthcare voice AI” and the distance between them is usually larger than the label implies. A documentation vendor and a patient-access vendor share almost nothing operationally. They sell to different buyers, solve different jobs, and own different data.

A documentation player lands through the CMIO and IT, rides the EHR relationship, and expands “up the chart” into coding and clinical documentation integrity. Its moat is note and coding accuracy at enterprise scale. A patient-access player lands through practice operations, owns the inbound and outbound phone line, and expands across the patient journey from scheduling to intake to payments. Its moat is the call channel plus specialty-specific workflow data. Compare, say, Abridge or Ambience on the documentation side with Assort or Phreesia on the access side: same two-word category, opposite businesses. They aren’t competitors today. Whether they stay in separate lanes is the open question the rest of this piece takes up.

The force that reshapes the board: EHR bundling

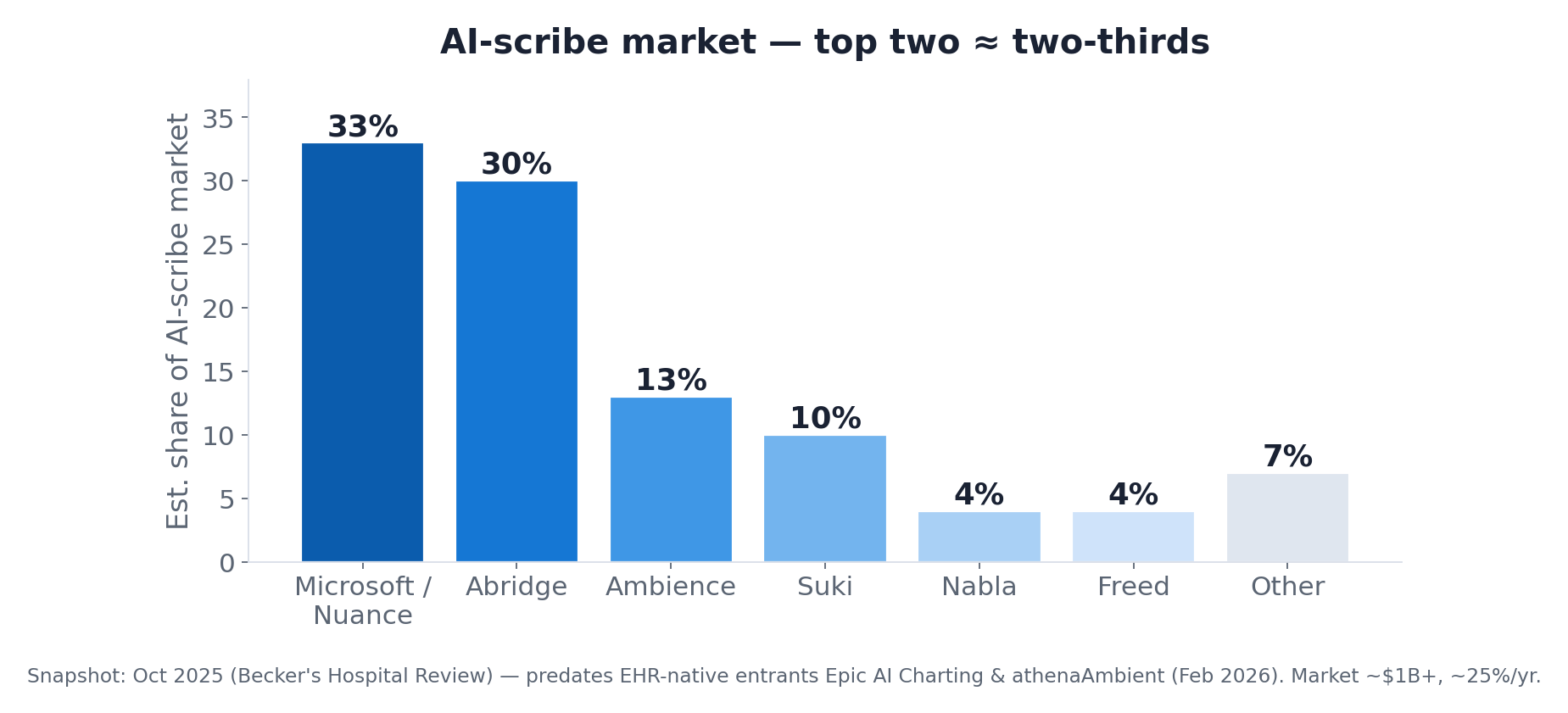

The biggest dynamic in 2026 is that the EHR vendors are shipping ambient AI natively. In February 2026, Epic released AI Charting (built on Microsoft’s Dragon ambient engine) into limited availability, and athenahealth launched athenaAmbient, free, inside the workflow, for its 160,000+ providers. When the system of record gives away a scribe that’s already in the chart, standalone documentation vendors charging $200 to $600 per clinician per month have to prove they’re materially better. MedCity News asked outright whether ambient-scribe startups “have a future now that Epic launched its own tool.”

This compresses the documentation lane hardest, which is why the market is consolidating there. The snapshot below is from late 2025, before the EHR-native tools arrived. Even then the top two vendors held roughly two-thirds of the market, and the EHR entrants only tighten the squeeze.

Bundling bites unevenly, though. Patient-access voice agents and payer-call automation work on a channel the EHR usually doesn’t control: the practice’s phone line, which sits on a separate telephony system rather than inside the record. Switching on a scribe in the chart is close to a settings change. Taking over a clinic’s inbound calls is a project. That gap is part of why capital keeps flowing into the patient-access and RCM lanes, and it points to the part most market maps skip.

Why the practice phone is hard to migrate

The phone line is sticky for an unglamorous reason. Moving it is a project. Plenty of independent and small-group practices still run on a plain landline or a wireless carrier rather than a modern cloud phone system with open APIs (Twilio, Zoom, RingCentral, Microsoft Teams Phone). Putting an AI voice agent in front of that line usually means porting the numbers, standing up VoIP/SIP, registering for 10DLC so appointment texts actually get delivered, wiring the agent into the EHR, rebuilding call routing and after-hours coverage, moving the contact list, and retraining the front desk on a new workflow. The 10DLC step alone can run for weeks. Every major U.S. carrier now blocks unregistered business texting, and healthcare messaging draws extra scrutiny.

All of that lands on a practice with no spare IT staff and no slack in the day. The owner is seeing patients and the office manager is already swamped, so even when the return is obvious the migration drags out both the sales cycle and the go-live date. I ran into this building the patient-facing assistant at KinDentists. The flip side is the interesting part. Once a vendor has done the work to get onto the phone line and into the workflow, the next vendor has to repeat all of it to displace them. The migration tax that slows the sale becomes a moat once you’re through it.

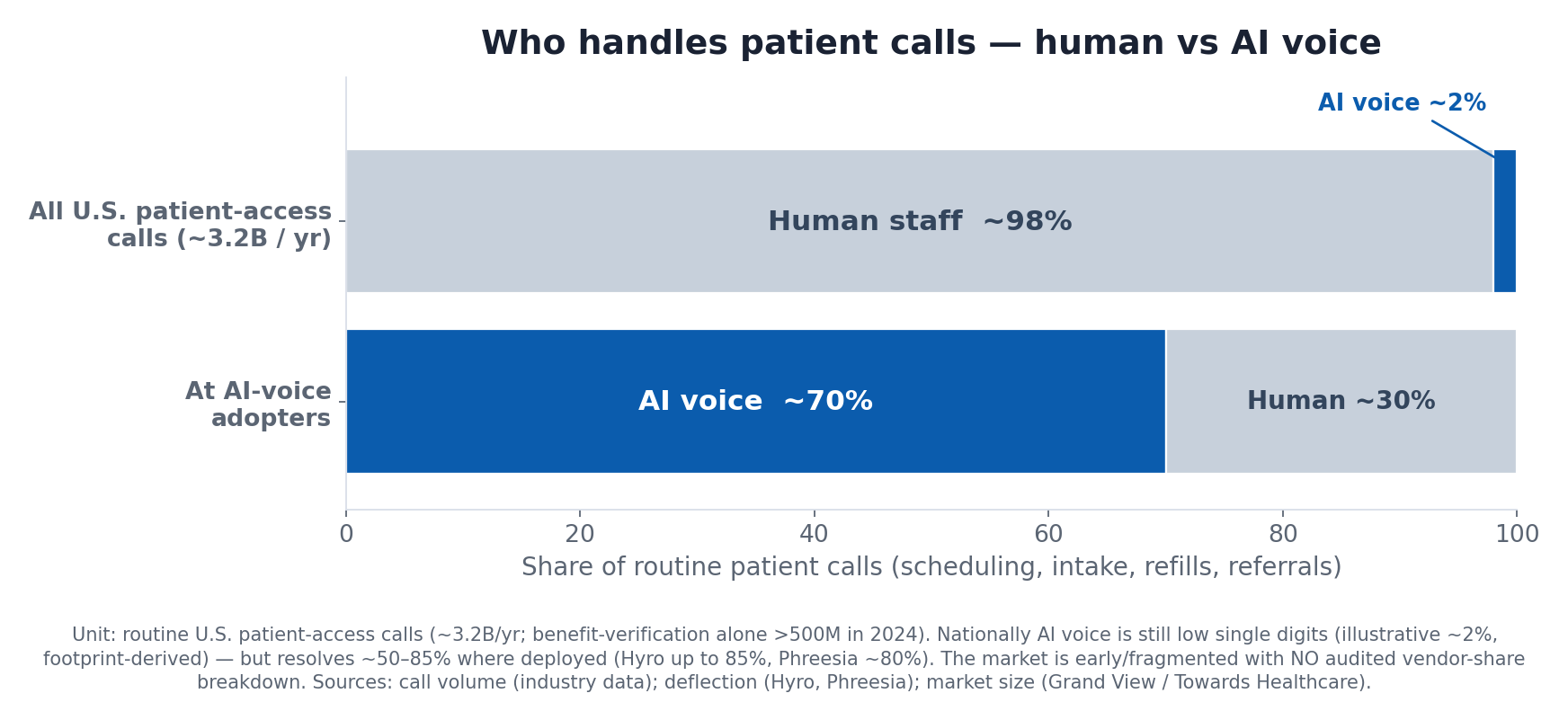

Patient access: earlier innings, still mostly human

Where documentation is consolidating, patient access sits roughly where the scribe market sat a few years ago: large, fast-growing, and fragmented, with no clear share leader yet. Most practices still run their phones on human staff. Where AI voice is deployed, it already resolves the majority of routine calls.

The AI-voice-in-healthcare market is roughly $0.5B in 2025 and growing about 38% a year. It’s smaller and much earlier-stage than ambient documentation, and far less settled. Real demand, fast growth, no entrenched leader, and a channel the EHR can’t easily absorb: that mix is what pulls in capital. It’s also why a distribution edge, getting onto many practices’ phone lines at once, matters more here than any single feature.

A caveat on “share.” For ambient scribing there’s market-research data; for the patient-access vendors there isn’t reliable, publicly available data yet. A high-level approximation is what the companies themselves have disclosed about their footprint, keeping in mind it mixes units (practices vs health systems vs interactions):

| Vendor | Primary buyer | Disclosed footprint | Note |

|---|---|---|---|

| Phreesia (VoiceAI) | Ambulatory + health systems | ~4,700 org clients (intake base) | Largest installed base; voice product is new (2025), voice-specific adoption undisclosed |

| Assort Health | Specialty group practices | Hundreds of practices, thousands of providers, 190M+ interactions | Specialty-specific, voice-native pure-play |

| Luma Health | Health systems and specialty | 50+ health systems | KLAS top performer in patient outreach |

| Hyro | Health systems | ~45 large systems | Voice and chat; millions of conversations |

| Hippocratic AI | Health systems and payers | 50+ systems / payers | Rooted in outbound clinical engagement; its 2026 “AI Front Door” extends into inbound access |

| Others | Varies | n/a | Notable, Orbita (Kore.ai), Simbo AI, plus traditional human answering-service / BPO incumbents |

Self-disclosed footprints, not measured market share, and the units differ. No reliable public vendor-share breakdown exists yet for patient-access voice AI. Sources: company disclosures, Becker’s, KLAS (2025 to 2026).

Everyone is widening toward the same center

The other throughline is that nobody wants to stay a point solution, and the tidy boxes above are already starting to blur. Abridge is pushing from notes into coding and revenue cycle and talks about an “operating system for medicine.” Ambience added coding and clinical documentation integrity. Commure already spans RCM and ambient. Microsoft is folding its tools under one Dragon Copilot. Assort began as a specialty scheduling agent and now markets a platform spanning intake, referrals, eligibility, refills, and payments.

Two forces turn that ambition into a pattern. The models underneath are commoditizing. Frontier capability is increasingly rentable by API, and the leading voice players are trained on similar orders of magnitude of data, each citing well over a hundred million patient interactions. Once model quality stops being the differentiator, the durable advantages shift to distribution, proprietary workflow data, and depth of EHR integration, the assets that take years rather than API calls to build. This is the familiar venture pattern in which distribution starts to beat product as the product gap narrows. The second force is plainer. A company raised at a valuation from roughly one to several billion dollars can’t justify it on a single workflow, so each is pushed to widen its footprint until it runs into the others.

The clearest current example is the one buyers keep asking about, Assort and Hippocratic. On paper they served different segments: Assort the specialty-practice front desk, Hippocratic outbound clinical engagement for health systems and payers. In 2026 both moved toward the middle. Hippocratic launched an “AI Front Door” that fields inbound scheduling, results questions, and billing in a single continuous patient conversation, with early deployments at systems including Cincinnati Children’s and UNC Health. That’s the inbound-access lane. Assort, after a $120M round, announced a push from ambulatory practices up into health systems, naming partners such as John Muir Health, and now runs a side-by-side page comparing itself to Hippocratic. One is coming down from clinical care toward the front door. The other is coming up from the front desk toward the enterprise.

How far this goes is unsettled, and worth not overstating. Patient access and clinical care management still sit in different budgets and different parts of the org chart. Practice operations and revenue cycle on one side, the chief nursing or medical officer and population health on the other. Healthcare integration is slow. The layers may well overlap at the edges while each keeps its core, the way documentation and revenue cycle have coexisted for years. The direction is clear enough that “who the AI talks to” is becoming a starting position rather than a fixed segment. Either way, the contested asset is the same: distribution across many sites, and the workflow data that accrues once a vendor is embedded, which is what the next section is about.

Where the distribution is going

That last point is underappreciated. Specialty practices are increasingly owned by private-equity-backed MSOs, the dermatology, orthopedics, gastroenterology, and oncology roll-ups, and healthcare PE set a record in 2025. At the MSO level, AI is bought once at the platform and deployed across affiliates, with platform-grade compliance. For any vendor selling into group practices, the fastest path runs through the handful of sponsors and platforms that already own them, not 200 individual offices. The winners in the patient-access lane will be the ones who build that channel deliberately.

The takeaway

If you only remember one thing: skip the question of which healthcare voice AI is best, and ask who the AI talks to. Documentation, patient access, and revenue cycle look similar from a distance and behave nothing alike up close. The buyer is different, the moat is different, and the exposure to EHR bundling is different. Lump them together and you’ll misread all three. The lines are beginning to blur as the best-funded players widen out, and even then the first question to ask about any of them is still who the AI is talking to.

Sources

Company disclosures and reporting (mid-2026): Abridge, Ambience, Assort Health, Microsoft/Nuance, Suki, Nabla, Corti, Heidi, Hippocratic AI, Hyro, Phreesia, Commure-Athelas, Infinitus. Epic AI Charting and athenahealth athenaAmbient launches (Healthcare IT Today, HLTH, TechTarget, MedCity News, February 2026). Becker’s Hospital Review (ambient-scribe market share, October 2025 snapshot). Patient-access and AI-voice market sizing (Grand View Research, Towards Healthcare) and deflection benchmarks (Hyro, Phreesia). Assort Health Series C and health-system expansion (Assort Health, HIT Consultant, Fierce Healthcare, June 2026); Hippocratic AI “AI Front Door” and health-system partnerships (PR Newswire, Business Wire, Fierce Healthcare, April 2026). Additional reporting from Fierce Healthcare, STAT, Fortune, and Sacra, plus healthcare-PE/MSO coverage (Becker’s ASC, GAO). Figures are directional and point-in-time.