The 2023 healthcare-AI map, three years later: who flourished, who flatlined

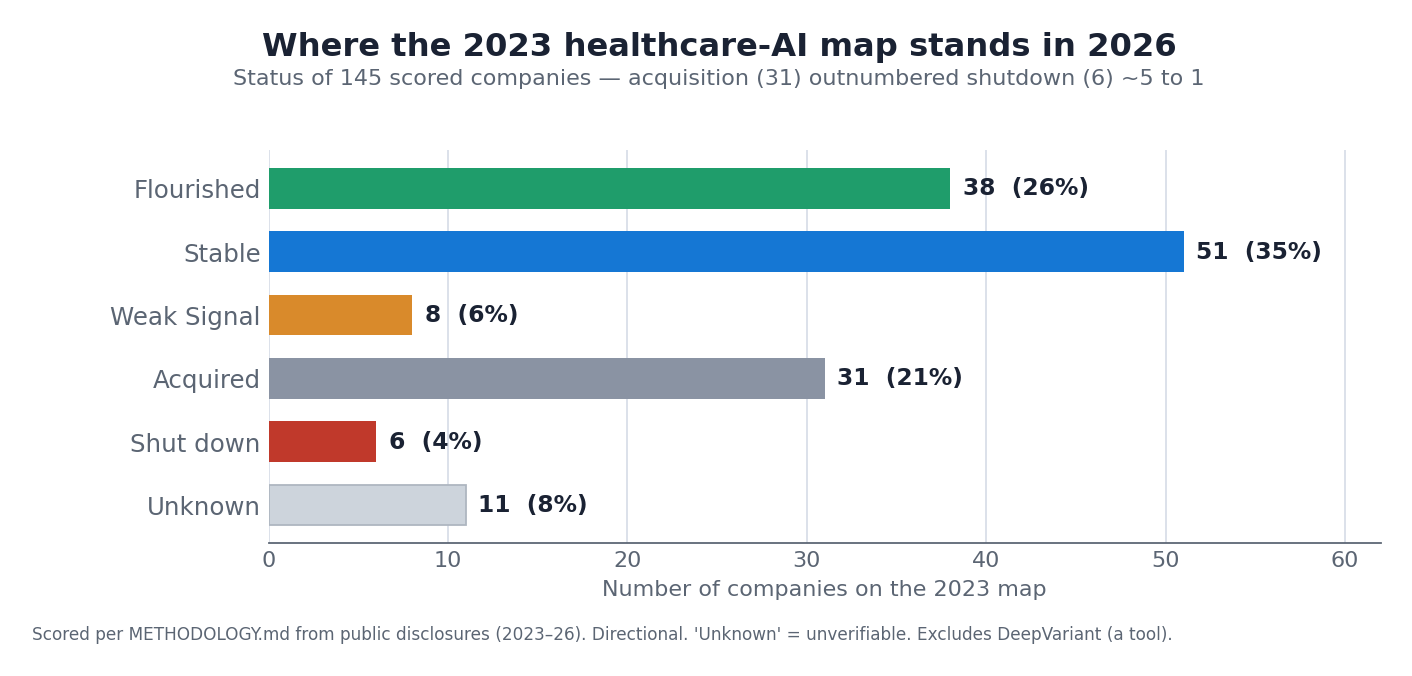

In June 2023, three authors mapped ~145 generative-AI healthcare startups. One of them, Jon Wang, then built Assort Health, now valued at $1.2B. We re-scored the whole map against public signals: about 38 flourished, ~31 were acquired, and only ~6 actually died. Here is what the three-year scorecard says about which healthcare-AI bets paid off.

How to read this. This is a three-year refresh of a specific, public artifact: the June 2023 market map in “Where Generative AI Meets Healthcare” by Justin Norden, Jon Wang, and Ambar Bhattacharyya. We transcribed all ~145 companies from the original map and scored each one’s 2026 status against an explicit rubric (see How these labels were scored, below). Statuses are editorial judgments and funding figures move monthly, so treat the pattern as the point, not any single cell. The scoring rule and confidence model are described below.

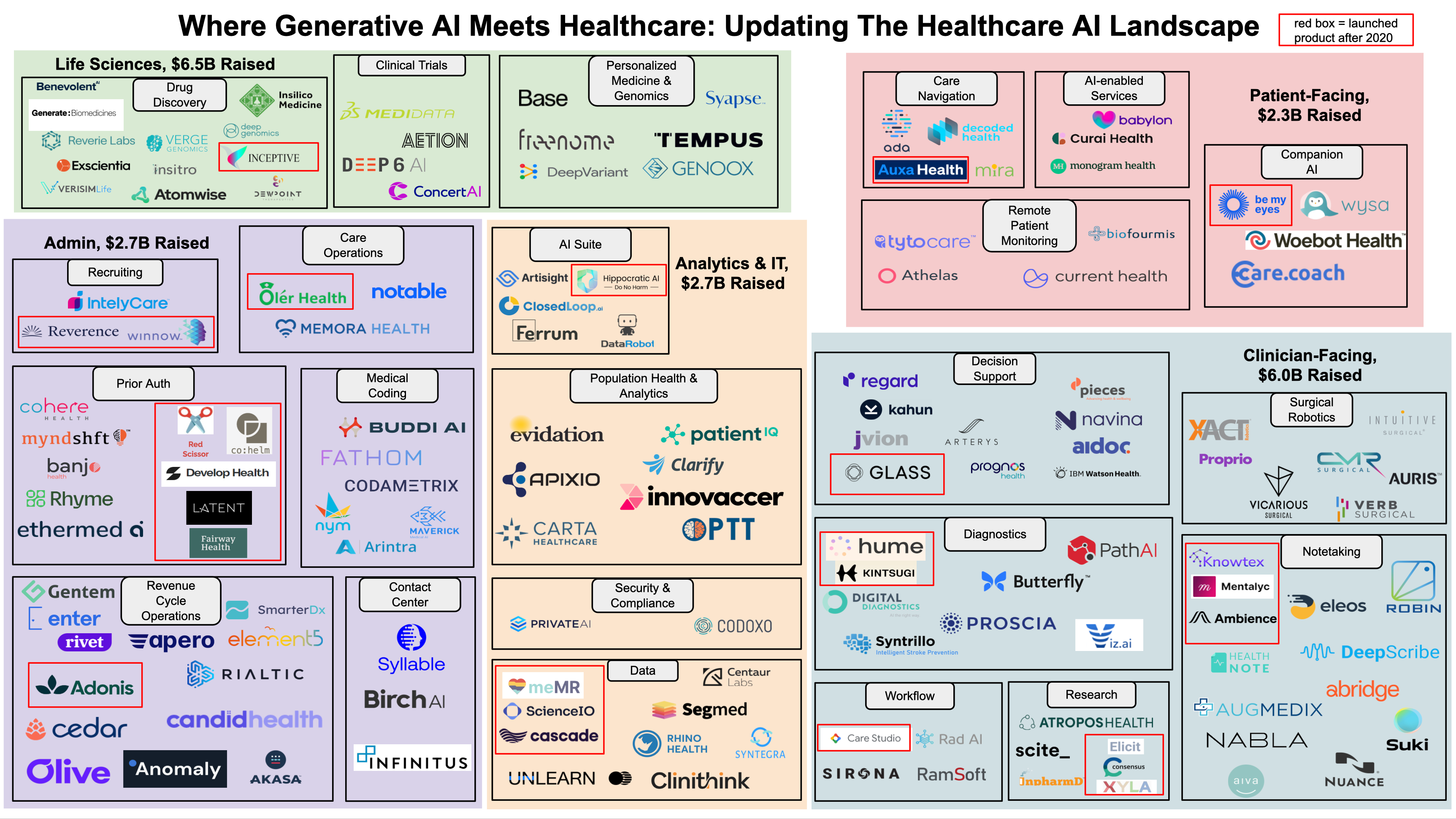

Three years ago, three authors drew a line around a fast-moving field and named names. Their map plotted about 145 generative-AI healthcare companies, collectively ~$20B raised and ~47,000 employees, across five sectors, and put a red box around every company that had “launched its product after 2020,” their proxy for AI-native. A map like this ages in public. That is what makes it worth revisiting.

One reason stands out. One of its three authors, Jon Wang, went on to co-found Assort Health, and on June 24, 2026, Assort raised $120M at a $1.2B valuation. The map records how one of its makers read the board right before he played it. We’ll come back to that.

Before scoring the companies, it helps to see the original artifact. It was a 2023 snapshot of where the authors saw generative AI showing up across healthcare, with red boxes marking companies whose products launched after 2020. That original framing is what makes the refresh useful: three years later, each logo has either compounded, been acquired, stalled, disappeared, or become hard to verify.

Source: Justin Norden, Jon Wang, and Ambar Bhattacharyya, “Where Generative AI Meets Healthcare”, June 2023.

First, the scorecard.

Most of the map is still standing

The dominant story of the past three years in tech has been “the AI bubble.” Under that story, a 2023 startup map would read as a graveyard by now. The record shows something else.

Of the 145 scored companies, roughly 38 clearly flourished (an IPO, a valuation step-up, or undisputed category leadership), about 51 are stable (still independent, operating on a normal cadence), 8 show a weak signal (a down round, layoffs, or a similar setback in the public record), 31 were acquired, 6 actually shut down, and 11 can’t be reliably verified at all. Outright death was among the rarest outcomes on the entire map, roughly one company in twenty-five. The far more common non-survival path was getting bought. That’s 31 acquisitions versus 6 shutdowns, about five to one.

That single ratio reframes the era. The 2023 to 2026 healthcare-AI story reads as a sorting, not a crash. Capital and customers concentrated around a smaller set of winners while the long tail got absorbed into larger platforms. The map didn’t burn down. It consolidated.

The refreshed map

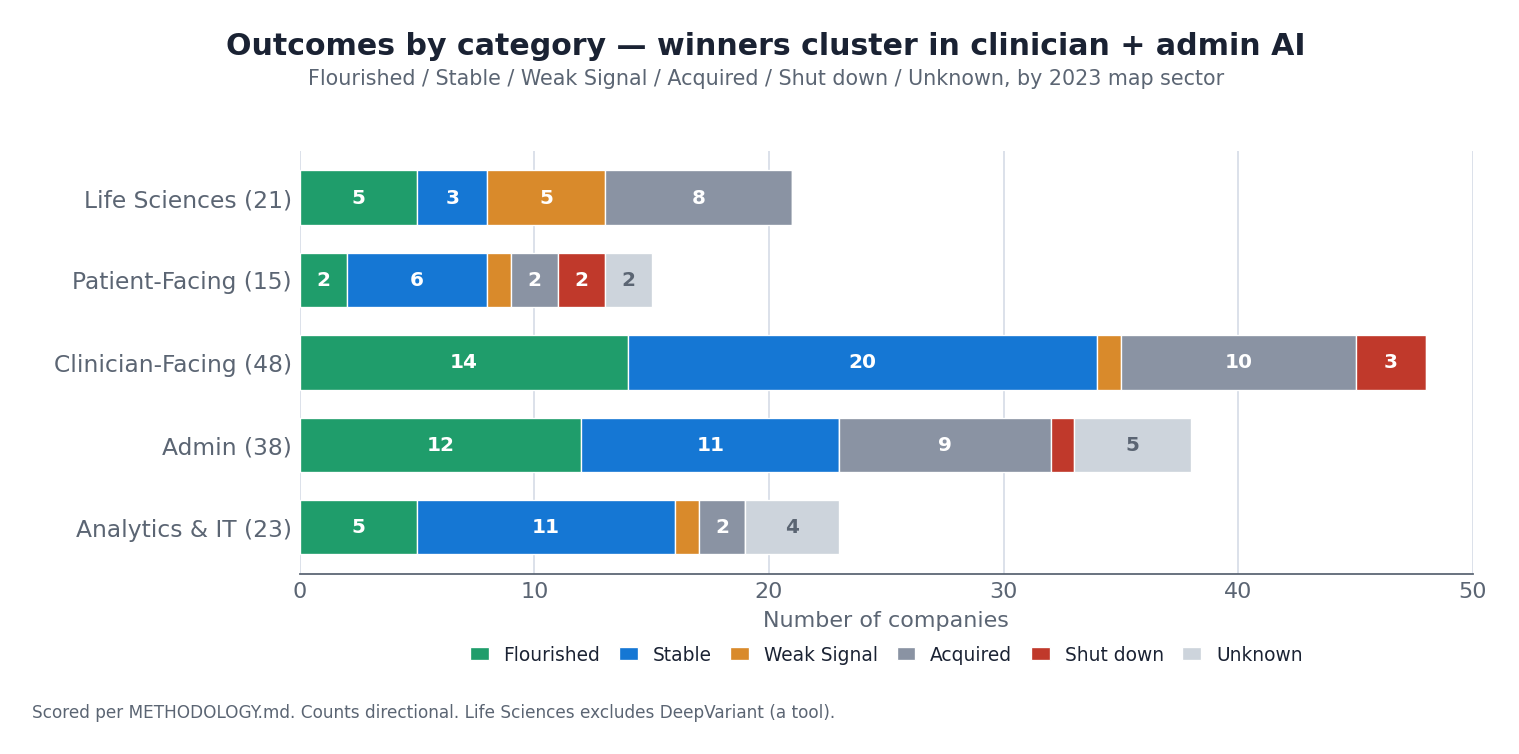

Here is the original map, re-colored by where each company sits today: green flourishing, blue stable, amber weak signal, grey acquired (acquirer noted), red shut down, and a dashed grey for names too sparse to verify. Within each sector, companies are ordered best-outcome first, so you can read each box’s “health” at a glance.

A few identity notes fall out of the refresh. Several “acquisitions” on the map had actually already happened by mid-2023. Nuance (Microsoft), Auris (J&J), IBM Watson Health (→ Merative), Base Genomics (Exact Sciences), and Medidata (Dassault) were legacy logos even when the map was drawn. Two names changed identity in ways worth knowing: co:helm is now Anterior, and the cryptic “Xyla” box turned out to be the most important cell on the entire map.

How these labels were scored

A “who flourished” verdict is only as good as its method, so here is the rule. The full version, with thresholds and confidence model, is available on request. Each company was scored on a panel of signals: most-recent funding round and stage, valuation direction versus the prior round, headcount or layoff events, traction or category-leadership proxies, and any structural event. It was then labelled by an ordered rule. Shut down and Acquired are factual. Flourished requires a hard positive, an IPO, a valuation step-up, or documented category leadership such as a Best-in-KLAS #1. Weak Signal requires at least one negative item in the public record (a down round, layoffs, a delisting, or a failed program) not offset by a recent up-round. Stable is an explicit residual, “operating, no qualifying signal,” and Unknown means the public record is too thin to call. Every label carries a High, Medium, or Low confidence, and only High- and Medium-confidence firms are used as named examples below. The per-company signals and sources behind each label are tracked separately and available on request.

Two things to keep in mind when reading the chart. The labels track public signals, so the bucket that carries the least information is Stable: companies operating independently with no scoreable catalyst in the record. That’s an absence of public news. Plenty of healthy, profitable, or heads-down firms raise quietly, or don’t need to raise at all, and they land in Stable by default. Weak Signal is narrower, at least one negative item in the public record such as a down round or layoffs. In a market that re-priced almost everything, that stays a data point. The labels are working judgments scored from the public record and revised as better evidence surfaces. The full rubric and per-company sources are documented separately.

What actually died, and the thing the deaths had in common

Six clear shutdowns, and they rhyme.

Babylon Health was the cautionary giant, a telehealth unicorn once valued near $2B that went bankrupt and was sold for parts in 2023. Woebot, a pioneer of the therapy chatbot, retired its consumer app in 2025, its founder noting that AI was moving faster than the regulators who’d have to bless it. Olive AI, the ~$4B “automate everything in the hospital” darling, wound down in late 2023 and sold its pieces to Waystar and others. Robin Healthcare (an ortho ambient scribe on dedicated hardware) ran out of runway in 2023. XACT Robotics (needle-steering hardware) couldn’t raise and shut down. Kintsugi, whose voice-biomarker science was genuinely novel, concluded the VC model didn’t work under FDA hurdles and open-sourced everything.

Line them up and the shared profile is unmistakable. The deaths clustered where a startup tried to replace the clinician or own the entire care stack (Babylon, Woebot), to boil the ocean of hospital admin on one platform (Olive), to win on capital-intensive hardware (XACT, Robin), or to sell regulated science with no reimbursement path (Kintsugi). Model quality is absent from that list. Every one of these companies shipped working AI. What killed them sat around the AI: the distribution, the focus, a payer who’d actually pay, none of which ever closed.

What flourished, and a quiet vindication of the “red box”

Now the other end of the map.

The winners cluster hard in clinician-facing and admin AI, and they share the opposite profile of the deaths: narrow job, clear buyer, obvious ROI. Most of them are also LLM-native, launched after 2020, which was the authors’ own “red box” hypothesis. Three years later it reads as a good call.

The standouts:

- OpenEvidence (the legal entity is “Xyla,” the inscrutable box in the research corner of the 2023 map) is now valued at $12B and used by ~65% of US physicians, arguably the single most valuable company anywhere on the map, and one nobody would have flagged as the leader in 2023.

- Abridge went from an early-stage scribe to a ~$5.3B valuation, the runaway leader of ambient documentation, with Ambience ($1.25B) and Nabla close behind.

- Hippocratic AI ($3.5B) and Innovaccer (~$3.45B) anchor the analytics/agent layer, though Innovaccer’s up-round sat alongside a 340-person layoff, a reminder that a flourishing company can still shed staff.

- Tempus IPO’d and Insilico pulled off Hong Kong’s largest 2025 biotech IPO, with AI-native biotech finally reaching public markets.

- And a deep bench of focused admin and imaging players raised strong rounds or won category leadership: Candid Health, Fathom, CodaMetrix, Cohere Health, Adonis, Infinitus, Latent, Aidoc, Viz.ai, Rad AI, and Navina.

What ties the flourishers together is distribution into a specific, paying workflow: the note, the code, the claim, the prior auth, the radiology read, the literature search. The further a company sat from a concrete reimbursable task, the choppier its three years.

The real headline: consolidation

Step back from the extremes and the middle of the map tells the biggest story. Roughly 31 of the 145 companies were acquired, about five times the number that died. This was the era of the strategic buyer and the PE roll-up.

A handful of acquirers show up again and again. Commure absorbed Athelas, Augmedix, and Memora into one platform. Tempus bought Arterys and Deep 6 AI. Datavant took Aetion (and a slice of Apixio). J&J folded Auris and Verb into its Ottava robot. Roche paid up to ~$1.05B for PathAI. CVS Health Ventures moved into Fathom and Codoxo. New Mountain Capital rolled SmarterDx into a ~$6B revenue-cycle platform. Even survivors are buying: IntelyCare acquired CareRev, Syllable bought Actium, Carta took Realyze. The 2023 map was a field of point solutions. The 2026 map is a smaller field of platforms assembling those points.

For a founder, that’s the quiet lesson hiding under the headline valuations. On this map, the most likely good outcome wasn’t becoming Abridge. It was getting acquired by something becoming Abridge.

The author’s tell: Jon Wang built in the emptiest cell

Which brings us back to where we started. When Jon Wang co-drew this map in 2023, the section that would become his own company was nearly bare. The patient-access and contact-center lane, AI that picks up the practice’s phone to schedule, triage, and take refills, held just a few names (Syllable, BirchAI, Infinitus), tucked in a corner while 48 companies crowded the clinician-facing box and 38 piled into admin.

The map’s own closing argument was that startups win through new markets, 10x improvements, and distribution: “the key to winning in healthcare is distribution, which is often the most challenging obstacle.” Wang then went and did exactly that, in one of the least-crowded cells he’d just drawn. Assort Health built the leader in specialty patient-access voice and, in June 2026, raised $120M at a $1.2B valuation, on the back of 190M+ patient interactions and 20x revenue growth in 15 months.

It illustrates the map’s deepest point. The crowded boxes, scribes, decision support, revenue cycle, produced most of the flourishers and most of the acquisitions, because that’s where attention and capital concentrated. An author who’d just spent months staring at where everyone else was building chose to go where they weren’t. Three years later, the contact-center corner has its own unicorn, several well-funded entrants, and a clear thesis. The map predicted its own blank space would fill in. One of its makers made sure he was the one filling it.

Takeaways

Four things to take from the refresh.

First, the “AI bubble” frame is wrong for this cohort. About 95% of the 2023 map is still operating in some form. The modal outcome was survival, and the second-most-common was acquisition. Hype corrected in valuations and headcount, and left the company count largely intact.

Second, focus beat ambition. The companies that died were the most ambitious: replace the doctor, automate the whole hospital, build the hardware. The companies that flourished did one reimbursable job extremely well. In healthcare, the narrow bet aged better than the grand one.

Third, “AI-native” was a real edge. The post-2020, LLM-native cohort the authors boxed in red is over-represented among the flourishers: OpenEvidence, Abridge, Ambience, Hippocratic, Latent, Anterior. Building on the new stack from day one mattered more than a head start with the old one.

Fourth, the map worked as a strategy. Read it as one of its own authors apparently did: the empty cells are the opportunity, distribution is the moat, and the most crowded box is rarely the best place to build. Assort is the proof of concept.

Sources & method

Original artifact: Norden, Wang & Bhattacharyya, “Where Generative AI Meets Healthcare,” AI Checkup (Substack), June 22, 2023. We transcribed all ~145 companies directly from the high-resolution market-map image, gathered a multi-signal panel for each from public disclosures (company announcements, Fierce Healthcare, STAT, TechCrunch, MedTech/Healthcare Dive, Crunchbase/PitchBook, SEC filings), collected June 2026, and applied a documented scoring rule. The full methodology (decision rule, confidence model, and known biases) and the per-company tracking table with sources are documented separately. Contact us for the methodology and underlying data. Status labels are editorial judgments; valuations are point-in-time and move monthly; 11 firms could not be verified and are marked Unknown. Figures are directional, so re-verify before citing.